Cross-border payments are an essential aspect of the global economy, enabling businesses and individuals to transact efficiently across national borders. However, the challenges posed by differing payment regulations and currency systems complicate these transactions, often hindering real-time payments. Industry experts suggest that emerging technologies like stablecoins and digital currencies could offer innovative solutions to streamline international money transfers, but regulatory hurdles remain a significant barrier. As countries increasingly explore digital currency initiatives, the potential for a more cohesive cross-border payments framework is on the horizon. Understanding the complexities of these processes is crucial for businesses looking to adapt and thrive in a rapidly evolving financial landscape.

The realm of international transactions encompasses various terminologies and practices, often referred to as cross-border payment systems or global money transfers. These activities hinge on the ability to send and receive funds across different jurisdictions while navigating the maze of distinct regulatory landscapes. In recent discussions, the integration of modern digital currencies and swift payment solutions has gained traction, especially as firms tackle the intricacies involved in executing prompt and efficient financial exchanges worldwide. Nevertheless, the debate surrounding the universal adoption of real-time payments and digital assets continues, revealing both the promise and the pitfalls of innovative financial technology. As we delve into this topic, we must consider the potential of both blockchain-based solutions and traditional banking systems in shaping the future of global financial transactions.

Applying for a merchant account is a crucial step for any business looking to accept card payments or other digital transactions. The first step in the application process typically involves selecting a payment processor that aligns with your business needs. Research various providers to understand their fee structures, supported payment methods, and customer service offerings. Once you’ve chosen a provider, visit their website to fill out an application form, which commonly requires basic information about your business, such as its name, address, contact details, and tax identification number. You may also need to provide information about your expected transaction volume and types, along with any required documentation that verifies your business operations.

After submitting your application, the payment processor will review the information and assess any risks associated with your business model. Depending on the provider and your business type, this process can take anywhere from a few hours to several days. Once approved, you will receive instructions on how to set up your account, including configuring your payment gateways, integrating with your website or point-of-sale system, and testing for functionality. For detailed insights on navigating payment processes, including the implications of new technologies like stablecoins in cross-border payments, check out the article on Payments Dive at https://www.paymentsdive.com/news/how-one-cross-border-payments-pilot-failed-real-time-stablecoins-rtp/804358/.

Understanding the Challenges of Cross-Border Payments

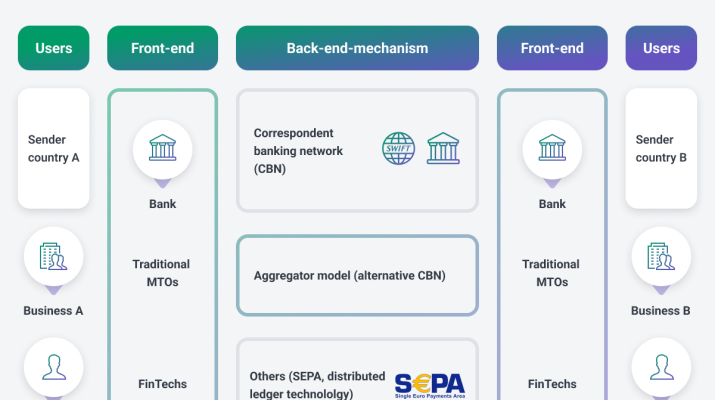

Cross-border payments are plagued by a multitude of challenges that stem largely from differing regulations and standards across countries. For instance, each country has its unique set of payment regulations that govern how money can be transferred, which creates a complex web of compliance requirements for financial institutions involved in international money transfers. As highlighted by industry experts, these variations lead to inconsistencies in service delivery and delays in transactions, as each country’s regulatory environment must be navigated carefully for effective operation.

Moreover, infrastructure is a crucial factor. While some countries have embraced technologies that enable real-time payments, others lag behind, lacking the necessary systems to facilitate these transactions. This disparity in technological advancements not only inhibits the speed of cross-border transactions but also increases costs. Therefore, before any real-time payment system can flourish globally, these regulatory and infrastructural barriers must be addressed comprehensively.

The Role of Real-Time Payments in Cross-Border Transactions

Real-time payments have the potential to revolutionize cross-border transactions by enabling instantaneous money transfers across borders. Networks such as the RTP (Real-Time Payments) system in the United States illustrate how efficient real-time processing can be integrated into international transactions. However, as discussed by The Clearing House’s Rusiru Gunasena, regulatory uncertainties and the lack of consistent rules across different jurisdictions impede the broader adoption of such systems. Without a robust framework that allows for seamless interoperability between national payment systems, the improvements promised by real-time payments remain out of reach.

Additionally, real-time payments can significantly enhance the customer experience by eliminating lengthy wait times often associated with traditional payment methods. Businesses and consumers alike stand to benefit from reduced settlement times, which can lead to improved cash flow and responsive financial operations. However, achieving a universally accepted framework for real-time cross-border payments requires collaboration among nations to harmonize regulations and establish common standards.

Navigating Payment Regulations Across Borders

Payment regulations present a formidable challenge in the realm of cross-border transactions. With each nation implementing its rules concerning currency controls, anti-money laundering requirements, and payment processing standards, achieving compliance becomes a complex endeavor for financial institutions. The discrepancies in regulations not only complicate the operational landscape but also create risks of non-compliance, which can lead to significant financial penalties and reputational damage.

For cross-border payments to be successful, there needs to be a concerted effort towards regulatory harmonization. As initiatives like the IXB pilot program demonstrated, without an agreement on regulations, interoperability between different payment systems remains limited. Collaborations between global payments organizations and regulatory bodies are essential to address these regulatory challenges and build a more cohesive framework that enables smoother international money transfers.

The Promise of Stablecoins in Cross-Border Payments

Stablecoins have emerged as a potential solution to streamline and reduce the costs associated with cross-border payments. Their value is pegged to stable assets such as fiat currencies, making them less volatile than other cryptocurrencies, thereby offering a more reliable payment method for international transactions. By leveraging blockchain technology, stablecoins have the ability to facilitate quicker transaction times and lower fees, which could significantly enhance the efficiency of cross-border payments.

However, the adoption of stablecoins is not without challenges. Regulatory scrutiny remains high, with different countries implementing varying degrees of restrictions and regulations on cryptocurrency use. While some nations explore the implications of a central bank digital currency (CBDC), others impose strict bans. As articulated by industry leaders, understanding and adhering to the differing regulatory landscapes is essential for businesses that wish to utilize stablecoins for cross-border transactions.

The Future of Digital Currency in Cross-Border Payment Solutions

Digital currencies, including cryptocurrencies and central bank digital currencies (CBDCs), have the potential to reshape cross-border payments fundamentally. As more than 130 countries explore the launch of their own digital currencies, we may see a new era characterized by more dynamic international financial systems that could bypass traditional banking hurdles. The advantage of digital currencies lies in their ability to facilitate quick transfers without needing numerous intermediaries, which can save both time and costs.

However, the future of integrating digital currencies into global financial systems also hinges on regulatory acceptance and technological advancement. As the landscape combines various digital assets and traditional payment rails, finding a balance between innovation and regulatory compliance will be critical. Collaborative frameworks that allow for digital currency usage while adhering to international standards for anti-money laundering and comprehensive payment regulations will be essential for driving widespread adoption.

Real-Time Payment Networks and Their Impact

Real-time payment networks, like the RTP system in the U.S. and the RT1 in Europe, have demonstrated that instant money transfers between accounts can revolutionize payment processes. These networks allow for almost instantaneous retrieval of funds, which can be crucial for businesses that rely on cash flow. However, the use of such networks for cross-border payments poses challenges, particularly due to the regulatory landscape that varies widely from region to region.

As these payment networks mature and new players enter the space, it’s vital for stakeholders to understand how these systems can interconnect. The success of any real-time payment initiative hinges not just on infrastructure but also on the capability to adapt to different regulatory requirements across jurisdictions. Stakeholders must collaborate to pave the way for innovative solutions that can transcend borders while conforming to local laws.

The Intersection of Technology and Compliance in Payments

The dynamic interplay between technology and compliance is particularly pronounced in the payments sector, especially with cross-border transactions that face numerous regulatory hurdles. As financial institutions advance their digital payment capabilities, they must simultaneously ensure compliance with diverse international regulations to mitigate risks and maintain operational integrity. This balancing act is essential for building trust and reliability in the cross-border payment ecosystem.

Integration of compliance technology can enhance the efficiency of processes like know-your-customer (KYC) and anti-money laundering (AML), helping institutions to navigate complex regulatory landscapes effectively. As institutions increasingly shift toward digital solutions, leveraging innovative compliance tools alongside advanced payment networks will be crucial for ensuring seamless international money transfers and fostering a compliant yet agile financial operation.

Evolving Consumer Expectations and Payment Innovations

Today’s consumers expect fast, efficient, and secure payment options, particularly in the context of cross-border payments. Traditional methods lacking the speed of real-time payment capabilities often leave customers frustrated. As digital currencies and stablecoins gain traction, consumer expectations are shifting towards solutions that not only meet their need for speed but also assure regulatory compliance and security.

Businesses must adapt to these evolving consumer expectations by leveraging innovative payment technologies. This involves investing in systems that can handle cross-border transactions more efficiently while guaranteeing compliance with international regulations. Establishing trust through transparency and security in transactional processes is paramount for companies seeking to maintain a competitive edge in the global marketplace.

Building Robust Infrastructure for Cross-Border Payments

The establishment of a robust infrastructure is critical for facilitating efficient cross-border payments. This entails not only technological enhancements but also the need for clear regulatory guidelines that can accommodate the complexities associated with international transactions. Successful payment systems integrate various operational components including payment networks, compliance measures, and customer service, ensuring seamless connectivity across borders.

Furthermore, investment in infrastructure is essential for aligning with the growing demand for real-time payment capabilities internationally. Stakeholders, including financial institutions and payment service providers, must collaborate to develop interoperable systems that can effectively manage the diverse challenges posed by differences in payment regulations and standards, thus paving the way for more efficient cross-border transactions.

| Key Points | Details |

|---|---|

| Cross-Border Payments Challenges | Differing regulations and lack of uniformity hinder real-time cross-border payments. |

| Regulatory Issues | Competing regulations across countries complicate money transfers. |

| Infrastructure Requirements | Both sending and receiving countries must have compatible payment infrastructures. |

| Pilot Program History | The Clearing House’s pilot with Swift faced regulatory challenges, leading to its pause. |

| Technical Hurdles | Different banking standards and AML regulations across countries add complexity. |

| Stablecoins as a Solution | While discussed as a simplification method, varying regulations still pose major issues. |

Summary

Cross-border payments continue to face significant obstacles, primarily due to varying regulations that complicate the instantaneous transfer of funds between countries. Despite efforts like the collaborative pilot by The Clearing House and Swift, which aimed to enhance cross-border payment efficiency, the initiative has been stalled due to regulatory and technical challenges. This complexity underscores the need for uniform standards and infrastructure development across nations to enable seamless and efficient cross-border payment systems.

Cross-border payments present a multifaceted challenge in today’s globalized economy, where individuals and businesses seek rapid and efficient international money transfers. The complexities of differing payment regulations across countries often hinder the potential for real-time payments, exposing the urgent need for a standardized approach to cross-border transaction processes. As digital currencies and stablecoins emerge as alternatives to traditional fiat systems, they could reshape the landscape of cross-border financial operations, although they still confront significant regulatory hurdles. For cross-border payments to thrive, collaboration and agreement between nations on payment infrastructure and compliance measures are essential. In an ever-evolving digital world, the future of international money transfer hinges on addressing these systemic challenges to pave the way for seamless, real-time transactions.

International fund transfers, also known as global remittances, embody the essence of cross-border payments by facilitating monetary exchanges between individuals and entities in different nations. The advent of technologies like digital currencies and stablecoins is revolutionizing these international financial interactions, offering new possibilities for efficient transactions. However, varied payment regulations across jurisdictions pose significant barriers, underscoring the necessity for harmonized frameworks. The pursuit of real-time transactions in this space illustrates the dynamic challenges faced by stakeholders in overcoming legal disparities and establishing a dependable payment infrastructure. Thus, as we explore the optimization of global remittances, it is crucial to consider both the technological advancements and the regulatory landscapes that interconnect these financial systems.

Frequently Asked Questions

What are cross-border payments and why are they important?

Cross-border payments refer to transactions where money is transferred from one country to another. They are important because they facilitate international trade, remittances, and investment, allowing businesses and individuals to conduct transactions across different currencies and jurisdictions.

What challenges exist in implementing real-time cross-border payments?

Real-time cross-border payments face numerous challenges, including differing regulatory frameworks across countries, lack of uniform rules, and varying standards like ISO 20022. These factors complicate the instant movement of money and require robust infrastructure in both sender and receiver countries.

How do payment regulations impact cross-border payments?

Payment regulations play a crucial role in cross-border payments by establishing the legal framework that governs transactions. Differences in regulations can lead to delays, increased costs, and complications in compliance, making it difficult to achieve efficient real-time payments across borders.

Can stablecoins enhance the efficiency of cross-border payments?

Stablecoins have the potential to enhance cross-border payments by providing a digital currency option that reduces transaction costs and speeds up processing times. However, varying regulations across countries still pose significant challenges to their widespread adoption for international money transfers.

What role do digital currencies play in cross-border payments?

Digital currencies, including central bank digital currencies (CBDCs), are being explored as an alternative for cross-border payments due to their potential for faster settlements and lower costs. However, regulatory obstacles and the need for interoperability between different digital currencies still need to be addressed.

Why did past projects, like TCH’s cross-border payment pilot, struggle to succeed?

Past projects, such as the TCH cross-border payment pilot, struggled due to a combination of competing national priorities, disparate payment regulations, and the lack of uniform technological standards. These challenges made it difficult to create a seamless real-time payment experience across borders.

What is the current status of real-time cross-border payment initiatives?

Currently, many real-time cross-border payment initiatives are on hold due to regulatory and technical challenges. However, there is ongoing activity and discussion among financial institutions and governments aimed at overcoming these obstacles to improve cross-border payment systems in the future.

How do currency regulations affect international money transfers?

Currency regulations affect international money transfers by imposing restrictions on currency exchange, transfer limits, and compliance requirements. These regulations can vary significantly by country, impacting the efficiency, cost, and speed of cross-border payments.

Real-time payments have transformed the way individuals and businesses conduct transactions. Unlike traditional payment methods that can take several days for funds to settle, real-time payment systems allow for immediate transfer of funds, greatly improving cash flow management for businesses and personal financial planning for consumers. This shift to instant payments also opens up new opportunities for innovation in banking and fintech, creating competitive landscapes where speed and service quality are essential.

Payment regulations have become increasingly important in the context of evolving payment technologies such as real-time payments and digital currencies. Regulatory bodies around the world are working to create frameworks that balance innovation with consumer protection and financial stability. As digital currencies and stablecoins gain traction, there is a pressing need for regulations that address issues such as fraud, money laundering, and the implications of cross-border transactions, ensuring that consumers and businesses are safeguarded in the digital economy.

International money transfers have traditionally been fraught with high fees and long processing times, but recent advancements in technology, including blockchain and stablecoins, are promising to revolutionize this sector. With digital currencies offering lower transaction costs and faster settlement times, individuals and businesses can send money across borders more efficiently than ever before. This is particularly beneficial for migrant workers sending remittances home, helping to ease the financial burdens for millions relying on these funds.

Stablecoins have emerged as a powerful tool in the digital currency landscape, bridging the gap between traditional finance and the innovative world of cryptocurrencies. Pegged to stable assets like the US dollar, stablecoins provide the benefits of digital currencies—such as speed and security—while minimizing the volatility typically associated with cryptocurrencies. This makes them a preferred choice for various applications, including remittances, online commerce, and even as a medium of exchange in global trade.

Digital currency adoption is on the rise, influencing global finance with implications for central banks, businesses, and consumers alike. As more entities explore the potential benefits of digital currencies, such as increased transactional efficiency and lower costs, the financial landscape is shifting. Central bank digital currencies (CBDCs) are also gaining attention as governments seek to harness the advantages of digital financial systems while maintaining regulatory oversight and consumer trust in their national currencies.

The failure of the cross-border payments pilot conducted by The Clearing House (TCH) underscores the complexities inherent in aligning various national regulatory frameworks. As Patrick Cooley reports from the Money 20/20 conference in Las Vegas, competing interests between countries, along with disparate regulatory standards, created significant hurdles in transitioning to instantaneous money transfers. Rusiru Gunasena, TCH’s head of business development, emphasized during the conference that for real-time payments to succeed internationally, an unprecedented level of regulatory alignment and robust infrastructure is required on both sides of the transaction. Unfortunately, the pilot’s inability to continue is a reflection of a broader market readiness issue rather than just technical capability.

Despite the enthusiasm surrounding the IXB pilot program launched in collaboration with SWIFT in 2022, it quickly became evident that the landscape for cross-border transactions is riddled with complications. The promise of revolutionizing cross-border payments faced immediate scrutiny as regulatory frameworks varied significantly among participating nations, leading to a halted initiative just a year later. Gunasena pointed out the diverse regulatory environments and compliance requirements that complicate any kind of cross-border transaction — from differing anti-money laundering standards to incompatible technical infrastructures like the ISO 20022 banking standard.

The suggestion that stablecoins could be a panacea for these issues has not materialized as hoped. Though they are designed to facilitate quicker and cheaper cross-border payments, they still face the same regulatory barriers that affect traditional fiat currencies. Gunasena highlighted that many governments, including those in China and Egypt, have imposed restrictions on cryptocurrency usage, thus limiting the effectiveness of stablecoins designed for international transfers. Furthermore, with around 130 countries exploring their own digital currencies, the fragmentation of digital fundraising adds yet another layer of complexity to cross-border transactions.

TCH’s recent experience serves as a reminder that while real-time payment networks hold significant potential, the roadmap to their global implementation is filled with regulatory challenges and practical limitations that cannot be overlooked. Gunasena expressed cautious optimism that advancements will eventually come, but the road to seamless cross-border payments remains long and fraught with obstacles. Without a unified framework that accommodates the needs and regulations of multiple jurisdictions, the dream of instantaneous global transactions may remain just that: a dream.