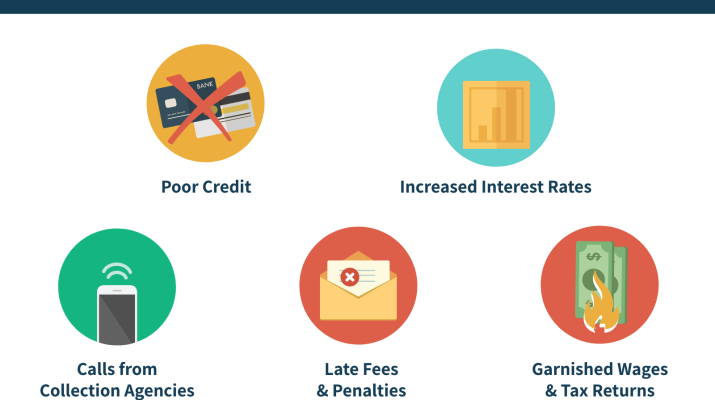

Student loan default can be a daunting reality for many borrowers, especially as the Department of Education has resumed sending defaulted student loans to collections. With the threat of garnished wages looming, it’s crucial for those struggling with payments to understand their options. If you find yourself significantly behind, immediate action is vital to avoid further financial repercussions. Defaulting not only impacts your ability to secure future loans but also negatively affects your credit score. Fortunately, there are viable paths like loan rehabilitation options and consolidation that can help you regain financial stability.

Falling behind on educational financing can lead to serious consequences, including collection efforts that might disrupt your life. When borrowers fail to meet their payment obligations, their accounts may go into a state known as default, which triggers a chain of negative outcomes such as student loan collections and garnished wages. To navigate this distressing situation, understanding the various strategies for recovery is essential. Whether considering direct loan consolidation or exploring how to avoid collections through loan rehabilitation, taking proactive steps can make all the difference. Addressing these issues head-on not only mitigates immediate threats but also lays the groundwork for a healthier financial future.

Understanding Student Loan Default

Student loan default occurs when a borrower fails to repay their student loans as agreed, typically after a significant period of non-payment, often 270 days. Defaulted student loans can have serious consequences, including negative impacts on credit scores and potential legal action by loan servicers. The Department of Education emphasizes that timely payment is critical, as defaulting puts borrowers at risk of losing their financial stability.

When loans go into default, borrowers lose eligibility for various repayment plans and assistance programs designed to ease the burden of student debt. Understanding the ramifications of student loan default is essential for borrowers to take proactive steps toward resolving their debts. Avoiding default requires continuous engagement with loan servicers and making timely payments.

Frequently Asked Questions

What should I do if I have defaulted student loans?

If you have defaulted student loans, it’s crucial to take immediate action. You can apply for Direct Loan Consolidation, enter a loan rehabilitation program, or consider paying off the entire balance to bring your loans out of default. Each option has its own requirements and consequences, so it’s essential to understand them fully before taking steps.

How can I avoid student loan collections on my defaulted loans?

To avoid student loan collections on defaulted loans, you should contact your loan servicer and explore options such as loan rehabilitation or consolidation. Taking proactive measures can prevent garnished wages and adverse effects on your credit score.

What are the loan rehabilitation options for defaulted student loans?

Loan rehabilitation involves making nine consecutive on-time payments based on your income, which can help remove the default status from your credit report. It’s a viable option to get your student loans out of default without wage garnishment for those who act quickly.

What happens if my student loans go into default?

When your student loans go into default, typically after 270 days of non-payment, the entire loan balance becomes due immediately. Additionally, your loan servicer can initiate collections, garnish wages, and report negatively on your credit history.

How can I check if my student loans are in default?

You can check if your student loans are in default by logging into your StudentAid.gov account or by contacting your loan servicer directly. This will help you understand your loan status and the necessary steps to take.

What does it mean if my wages are being garnished due to student loan default?

If your wages are being garnished due to student loan default, it means that a portion of your paycheck is being withheld to repay your debts. This typically occurs after loan servicers have initiated collection procedures following a prolonged default.

Can I remove the default status from my credit report?

Yes, you can remove the default status from your credit report by successfully completing a loan rehabilitation program or consolidating your defaulted loans. However, the process requires timely payments and may take some time.

What are the consequences of defaulted student loans on my credit score?

Defaulted student loans can significantly harm your credit score, making it difficult to obtain new credit or loans. Payment delays can begin affecting your credit report after 90 days, with default status being reported after 270 days.

Is it possible to repay defaulted student loans in full to avoid collections?

Yes, you can repay your defaulted student loans in full within 65 days of receiving the default notification to avoid collections and prevent further negative credit reporting.

How does the government handle student loan collections?

The government can send defaulted student loans to collections, which may involve legal actions to recover owed payments, including garnishing wages and seizing tax refunds if necessary.

| Key Point | Details |

|---|---|

| Risk of Collections | Defaulted student loans may be sent to collections, risking wage garnishment. |

| Default Status | Loans become delinquent after 90 days and enter default after 270 days. |

| Impact on Credit Score | Default status negatively impacts credit scores. |

| Actions Required | Borrowers must act quickly to avoid collections by contacting the Default Resolution Group. |

| Options to Resolve Default | 1. Direct Loan Consolidation 2. Loan Rehabilitation 3. Pay Off Entire Balance |

Summary

Student loan default poses a serious threat to borrowers, as defaulted loans can lead to collections, wage garnishment, and damaged credit scores. With over 5 million borrowers facing default, it is crucial to understand the available options to remedy this situation. Taking proactive measures such as loan consolidation, rehabilitation, or paying off the debt can prevent further financial consequences. Quick actions are necessary to avoid the harmful impacts of student loan default.

Student loan default occurs when a borrower fails to make payments on their federal student loans for an extended period, typically 270 days. When a borrower defaults, the entire loan balance may become due immediately, and the borrower faces severe consequences. These can include damage to their credit score, wage garnishments, and the loss of eligibility for further federal financial aid. To avoid these serious repercussions, it is crucial for borrowers to take action before falling into default.

If you are struggling to keep up with your student loan payments, consider reaching out to your loan servicer as soon as possible. They can provide vital information on your repayment options, including income-driven repayment plans that can lower your monthly payment based on your earnings. Additionally, if you find yourself experiencing financial hardship, you may qualify for deferment or forbearance, which temporarily pauses your payments without worsening your default status.

Another proactive step is to stay informed about your loans. Regularly check your loan status, and make sure you know the terms and conditions, including interest rates and repayment schedules. Set up automatic payments or reminders to ensure you never miss a due date. If you have multiple loans, consider consolidating them to simplify your payments and potentially lower your monthly obligations. Each of these actions can significantly reduce the risk of defaulting and help protect your financial future.

In cases where borrowers have already defaulted, it’s important to act quickly to rehabilitate your loans. Options include loan rehabilitation, which can help restore your loans to good standing after making a series of on-time payments. Alternatively, you may consider loan consolidation, which can help you manage your debt more effectively. Each of these steps requires communication with your loan servicer and a commitment to regaining control of your student debt.

Defaulted student loans occur when a borrower fails to make payments for an extended period, typically 270 days or more. When a student loan defaults, it can lead to severe consequences, including damage to the borrower’s credit score, inability to access further financial aid, and potential legal action from lenders. It’s crucial for borrowers to understand the implications of defaulting and to address their loans proactively before they reach this stage.

For those with defaulted student loans, loan rehabilitation options are available that can help borrowers regain their good standing. Loan rehabilitation typically involves making a series of agreed-upon payments over a specified time period, after which the default status is removed, and the borrower can begin to rebuild their credit. This process often requires communication with the loan servicer to establish a feasible payment plan and comply with all requirements to complete the rehabilitation successfully.

Student loan collections can be a daunting experience for borrowers. Once loans enter collections, they may be handed over to third-party collection agencies, which often use aggressive tactics to recover the owed money. It’s essential for borrowers to know their rights during this process, such as verifying the debt and understanding their options for negotiating repayment plans. Awareness of the Fair Debt Collection Practices Act can empower them to respond appropriately to collectors.

To avoid collections on student loans, borrowers should take proactive steps such as setting up automatic payments, seeking deferments or forbearances in case of financial hardship, and staying in regular contact with their loan servicer to discuss any issues that may arise. Additionally, borrowers should consider consolidating their loans to simplify their payment structure and potentially lower their monthly payments, thus reducing the risk of falling behind.

Garnished wages are one of the potential consequences of defaulting on federal student loans. If a borrower defaults, the government has the authority to garnish wages without a court order, which can lead to a significant reduction in take-home pay. To avoid this situation, borrowers should explore options like loan rehabilitation or consolidation before defaulting. Staying informed about debt management and repayment solutions can help prevent wage garnishment and provide financial stability.