The US payments systems are undergoing a significant transformation, fueled by the increasing adoption of electronic payments across various sectors. Recent trends indicate that organizations are moving away from traditional payment methods, with the Automated Clearing House (ACH) network reporting a 5.2% rise in transactions in the last quarter alone. This shift is set against a backdrop of innovations like the RTP Network and the newly launched FedNow service, both of which offer instant payments that enhance transaction efficiency. As financial institutions ramp up their engagement with these systems, understanding the dynamics of US payments systems becomes crucial for businesses navigating this evolving landscape. With an emphasis on seamless transactions, the push towards digital payments is reshaping how money moves in America, reflecting a broader global trend towards cashless economies.

In recent years, the landscape of American financial transactions has been increasingly dominated by digital methodologies, marking a shift away from conventional cash and checks. The innovative frameworks, such as the Automated Clearing House (ACH) and real-time payment infrastructures like RTP Network and FedNow, have revolutionized how consumers and businesses manage their monetary exchanges. These modern payment platforms facilitate expedited transactions and promote financial inclusion across a broader range of institutions. As the push for electronic payments grows, it also highlights the importance of understanding these evolving systems in the larger context of economic growth and operational efficiency. Thus, exploring the intricacies of US payment infrastructures unveils the significant strides being made towards instant and reliable financial transactions.

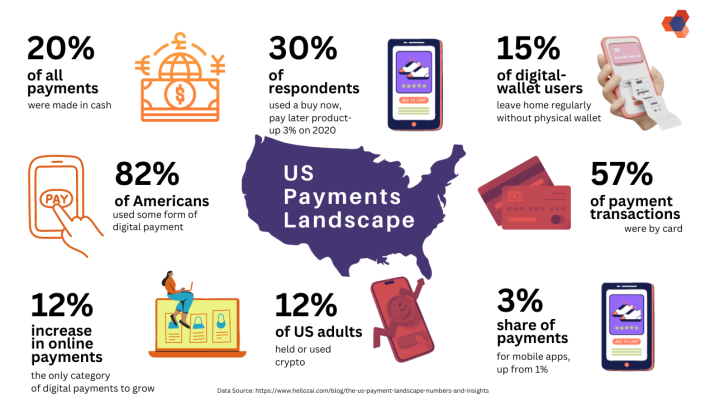

Growth of Electronic Payments in the U.S.

The recent statistics reported by Nacha illustrate a robust growth in the realm of electronic payments within the U.S. Automated Clearing House (ACH) transactions have increased by 5.2%, with a total of 8.8 billion transactions recorded in the third quarter alone. This surge can be attributed to various sectors, including internet and healthcare, where digital transactions are becoming the preferred method of payment. The dollar value associated with these transactions also experienced a notable rise of 8.2%, amounting to an impressive $23.2 trillion. As the country transitions toward a cashless society, electronic payments are becoming an integral part of everyday transactions, driving financial innovation across multiple industries.

Moreover, the trend towards embracing electronic payments is highlighted by the ongoing shift away from traditional payment methods such as paper checks. As more businesses recognize the efficiency and convenience that electronic payments offer, it fosters a more streamlined and secure transaction environment. This projected growth in electronic payment methods aligns with global trends, as countries worldwide increasingly rely on digital financial solutions, making it imperative for the U.S. to revamp its payment ecosystem for enhanced efficiency.

The Rise of Real-Time Payments: RTP Network Insights

The Clearing House’s RTP Network has recently made headlines with its significant milestone of processing 1.8 million transactions in a single day, valued at $5.2 billion. This achievement demonstrates the network’s capability to handle large volumes of real-time payments seamlessly, reinforcing its position as a leader in the rapidly evolving payments landscape. As financial institutions increasingly adopt real-time capabilities, the RTP Network is positioned well to meet the growing demand for instantaneous transaction processing. The leap in transaction volumes is not only a testament to the reliability of the network but also illustrates the financial sector’s shift towards embracing faster payment solutions.

As the RTP Network continues to gain traction, its competitive edge primarily arises from being the pioneer in real-time payment solutions. Introduced in 2017, it has set a benchmark for speed and efficiency in money transfers. The growing adoption of the RTP Network signifies a fundamental change in how individuals and businesses conduct transactions, prompting other payment systems, including FedNow, to enhance their offerings to attract customers. With U.S. payment systems rapidly evolving, the RTP Network’s success serves as a catalyst for future innovations in electronic payments.

FedNow: A New Player in Instant Payments

The Federal Reserve recently launched FedNow, an instant payments system designed to facilitate more efficient payment processing for all U.S. banks and credit unions. With an impressive 1,500 institutions already onboarded, FedNow represents a significant move towards modernizing the payment infrastructure in the United States. Its establishment aims to level the playing field, allowing smaller financial institutions, which have traditionally lagged behind, to compete effectively in the burgeoning real-time payments ecosystem. FedNow specifically addresses the challenges that these institutions faced in adopting existing systems like the RTP Network.

While the RTP Network has established itself as a robust option for real-time payments, FedNow’s focus on inclusivity may provide it with a unique opportunity to capture a broad user base. By appealing to smaller banks and credit unions that may not have the infrastructure to join larger networks, FedNow can effectively increase the accessibility of instant payment solutions. The introduction of FedNow not only enhances competition among U.S. payment systems, but also expands the potential for innovative financial technologies, leading to improved consumer and business experiences in electronic payments.

The Competitive Landscape of U.S. Payment Systems

As the landscape of U.S. payment systems evolves, the competition between the RTP Network and FedNow is intensifying. Each system seeks to persuade financial institutions to transition from traditional methods to more advanced electronic payment solutions. The clear advantage that RTP holds due to its head start in 2017, along with its backing from larger banks, creates a formidable challenge for FedNow. However, FedNow is strategically targeting smaller institutions, trying to offer tailored solutions that address their specific needs, which could change the game in the real-time payments space.

Furthermore, the competitive dynamics between these systems have significant implications for businesses and consumers alike. With increased competition, there is a growing opportunity for more innovative payment solutions that can enhance user experiences. As financial institutions adapt to these changes, they must weigh factors such as transaction speed, cost, and customer service in their decision-making processes. As both RTP and FedNow continue to innovate and refine their offerings, they will play a crucial role in shaping the future of electronic payments in the U.S.

Boosting B2B Transactions Through ACH

The rise in business-to-business (B2B) transactions via the ACH network underscores the increasing importance of electronic payments in facilitating smooth financial dealings among companies. In the third quarter, B2B transactions grew by 10%, reflecting a shift in how businesses manage their payments. This segment alone accounted for approximately 2.1 billion payments, with a total value of $16 trillion. Such significant participation in the ACH network highlights its effectiveness as a reliable payment method, enabling businesses to process payments quickly and securely.

As B2B companies embrace ACH for their transactions, they are discovering various benefits, such as lowered costs and increased efficiency. The trend indicates that more businesses are forgoing traditional practices in favor of digital alternatives that minimize the risk of fraud and delays associated with paper checks. The consistent growth in B2B ACH transactions not only signals a maturation of electronic payment systems but also reflects an evolving approach to commerce where speed and reliability are paramount.

The Impact of Healthcare Payments on ACH Growth

Healthcare payments represent a crucial driver of growth within the ACH network, evidenced by a 6.8% increase in healthcare transactions this year. As the healthcare industry relies on timely payments for services rendered, electronic payments have emerged as the most efficient solution. With 141 million transactions processed via ACH in this sector, the reliability and speed of electronic payments facilitate better cash flow management for providers looking to streamline operations.

Moreover, as healthcare organizations continue to address the challenges of cost management, implementing ACH payments offers numerous advantages that traditional methods cannot match. Electronic payments reduce administrative burdens and enhance patient experiences during the billing process. As more healthcare providers recognize the benefits of ACH, it further reinforces the pivotal role that electronic payment systems play in optimizing operational efficiencies across industries.

Consumer Preferences Shifting Towards Instant Payments

There is a noticeable shift in consumer preferences towards instant payments, as evidenced by the rising popularity of peer-to-peer (P2P) payment applications and services. The recent surge of 22.7% in peer-to-peer ACH payments to 122.2 million transactions underscores the growing desire for faster, more convenient payment options. Consumers are increasingly prioritizing speed over traditional methods, which typically involve longer settlement times and potential delays.

This changing landscape presents new opportunities for financial institutions to cater to consumer demands for instant payment solutions. As more individuals become accustomed to using platforms that offer real-time payment capabilities, the expectations for quicker settlements will undoubtedly rise. Adapting to this shift will be vital for U.S. payment systems to remain competitive, and it highlights the need for continuous innovation in electronic payments.

Integrating Digital Payments with Banking Systems

As the demand for electronic payments grows, integrating these systems into traditional banking infrastructures has become imperative. Institutions must find ways to marry existing banking systems with modern electronic payment solutions like ACH and real-time payment networks. Such integrations not only enhance user experiences but also drive operational efficiencies within financial institutions, enabling them to provide better services to their customers.

Addressing the challenges of integrating digital payment solutions involves reevaluating how banks approach technology adoption. By investing in robust infrastructures that support both instant and traditional payment methods, banks can ensure that they are well-positioned to meet the evolving preferences of consumers and businesses alike. This shift towards a more digital-centric banking environment reflects a broader trend in the finance industry to cultivate adaptability, innovation, and user-friendly services.

Future Developments in U.S. Payment Systems

Looking ahead, the evolution of U.S. payment systems is expected to accelerate as technology continues to advance. With both RTP and FedNow pushing for a larger share of the real-time payments market, we can anticipate further innovations in payment processing. Key players in the industry will likely focus on enhancing transaction security and improving user experience, ensuring consumers and businesses feel confident in their electronic payment choices.

Additionally, as international payment standards evolve, the U.S. may adapt its systems to remain competitive on a global scale. The incorporation of advanced technologies such as blockchain could also pave the way for new possibilities in electronic payments, ensuring that U.S. payment systems not only thrive domestically but also set benchmarks for international practices. The continued collaboration between stakeholders in the payments landscape will be crucial for navigating these challenges and opportunities.

Frequently Asked Questions

What are US payments systems and how do they work?

US payments systems refer to the networks and technologies that facilitate electronic payments across the country. This includes systems like the Automated Clearing House (ACH) network, which processes both credit and debit transactions, and instant payment systems like the RTP Network and FedNow. These systems allow for quick, efficient transfer of funds electronically, reducing the reliance on paper checks.

How is the ACH network relevant in US payments systems?

The ACH network is a significant component of US payments systems, providing a platform for processing electronic payments such as direct deposits and bill payments. Recent reports show a 5.2% increase in ACH transactions, reaching 8.8 billion, which reflects its growing importance in facilitating business-to-business transactions and everyday consumer payments.

What is the RTP Network and what role does it play in US payments systems?

The RTP Network, operated by The Clearing House, is a real-time payments system that allows for immediate fund transfers between banks. It recently achieved a record, processing 1.8 million transactions in a single day. The RTP Network aims to modernize US payments systems by offering faster transaction times compared to traditional methods, appealing to various sectors including businesses and consumers.

What is FedNow and how does it compare to other US payments systems?

FedNow is the Federal Reserve’s instant payment system launched in July 2023, aiming to facilitate real-time payments to consumers and businesses. It competes with the RTP Network by attracting smaller financial institutions that may be hesitant to adopt existing systems. With over 1,500 banks and credit unions already involved, FedNow is expected to significantly shape the landscape of US payments systems.

What trends are driving the growth of electronic payments in US payments systems?

The growth of electronic payments within US payments systems is driven by increased transaction volumes in sectors like healthcare and internet services. Notably, B2B transactions through ACH have risen by 10%, reflecting businesses’ preference for electronic payment methods over traditional checks, making electronic payments more streamlined and efficient.

What challenges do US payments systems face in transitioning to digital payments?

Despite the growing adoption of electronic payments systems, challenges remain in convincing many US financial institutions and businesses to transition from traditional payment methods to digital systems. Factors include concerns over security, integration costs, and the comfort level with established processes. Initiatives like FedNow are targeting these concerns by offering tailored solutions for smaller institutions.

What are the advantages of using instant payments like RTP and FedNow in US payments systems?

Instant payments through systems like RTP and FedNow provide several advantages, including immediate fund availability, reduced transaction times, and enhanced cash flow for businesses. They also improve payment efficiency and customer satisfaction by enabling quick transactions, marking a significant shift in how payments are processed in the digital age.

| Key Point | Details |

|---|---|

| Increase in ACH Transactions | 5.2% increase in ACH payments in Q3, totaling 8.8 billion transactions valued at $23.2 trillion. |

| RTP Network Records | On October 3, RTP processed 1.8 million transactions totaling $5.2 billion. |

| FedNow Participation | FedNow has attracted 1,500 banks and credit unions since its launch in July 2023. |

| B2B Transaction Growth | B2B ACH transactions increased by 10%, accounting for 69% of total ACH value. |

| Challenges for Instant Payments | FedNow aims for small institutions, facing challenges against larger competitors like RTP. |

| Peer-to-Peer Payments | Peer-to-peer payments surged by 22.7%, totaling 122.2 million transactions. |

Summary

US payments systems have experienced significant growth, as evidenced by the upward trend in electronic payments, particularly through the ACH network, RTP, and FedNow. The increase in transaction volumes across sectors signals a pivotal shift towards digital payment methods, aligning with global trends. As more financial institutions adapt to these systems, the dependence on traditional payment methods continues to dwindle, emphasizing the importance and future of US payments systems.

Source: https://www.paymentsdive.com/news/us-payments-systems-mushroom/803238/

Electronic payments have transformed the way we conduct transactions today, providing a convenient and efficient alternative to traditional cash payments. These digital transactions include various methods such as credit and debit cards, mobile wallets, and bank transfers, enabling consumers and businesses to exchange money quickly and securely from anywhere in the world.

The ACH network, or Automated Clearing House, serves as a key component of the electronic payments landscape in the United States. It facilitates the batch processing of debit and credit transactions, allowing for the transfer of funds between bank accounts electronically. This system is widely used for recurring payments such as payroll and bills, offering a reliable method for managing day-to-day financial activities.

Instant payments represent a significant advancement in the realm of electronic transactions, enabling funds to be transferred and made available to the recipient almost immediately. This capability is not only beneficial for consumers who want quick access to their money but also for businesses that require fast and efficient payment solutions to enhance cash flow and customer satisfaction.

The RTP Network (Real-Time Payments) is one of the leading platforms for instant payments in the United States. Launched by The Clearing House, this system allows banks to offer real-time payment services, enabling users to send and receive money instantly, 24/7. This innovation has brought about a more dynamic financial landscape, catering to the demands of an increasingly digital economy.

FedNow is another pivotal initiative aimed at enhancing the payment ecosystem. Developed by the Federal Reserve, FedNow is designed to provide a real-time payment service that supports instant transactions, fostering greater efficiency across the financial system. With the introduction of FedNow, all U.S. banks, regardless of size, can participate in real-time transactions, promoting inclusivity and speeding up the overall pace of financial exchanges.

Applying for a merchant account is an essential step for businesses looking to accept credit and debit card payments from customers. To begin the process, you should first research various payment processors to find one that suits your business needs. Consider factors such as transaction fees, monthly charges, and the types of payment methods supported. Once you have selected a payment processor, you will typically need to fill out an online application form where you will provide information about your business, including your business structure, estimated monthly sales volume, and the types of products or services offered. It’s also important to prepare necessary documents, such as your business license, tax identification number, and personal identification, to expedite the approval process.

After submitting your application for a merchant account, the payment processor will conduct a review to evaluate the risk associated with your business and transaction volume. This may involve checking your credit history and verifying your information to ensure compliance with industry regulations. Be prepared to provide additional documentation if requested. Once your application is approved, you will receive your merchant account details, which usually include a merchant ID and access to a payment gateway for transactions. To learn more about the various factors impacting the merchant account application process and the latest trends in US payment systems, visit Payments Dive for comprehensive insights: https://www.paymentsdive.com/news/us-payments-systems-mushroom/803238/.