The open banking rule is currently under scrutiny as the Consumer Financial Protection Bureau (CFPB) seeks public input for its revision, having received about 14,000 comments from various stakeholders. This regulatory framework is designed to enhance competition in the financial services sector by enabling consumers to share their banking data securely with third-party providers. Amidst the ongoing debate, banks and fintech companies find themselves at odds over how this rule influences consumer rights to manage personal financial information. The CFPB, under the guidance of the 2010 Dodd-Frank Act’s Section 1033, aims to create a transparent ecosystem that benefits consumers while being mindful of innovation within the financial technology landscape. As discussions evolve, the impact of fintech regulations and the role of the Consumer Financial Protection Bureau remains critical to shaping the future of digital banking in America.

The regulation known as open banking has emerged as a pivotal topic within the realm of financial services, particularly as the CFPB invites stakeholders to weigh in on potential revisions. This initiative focuses on allowing consumers the freedom to share their financial data with various entities, including innovative fintech firms that are reshaping how financial transactions occur. Sources from diverse industries, from advertising to retail, have submitted their opinions, reflecting a broad spectrum of interests affected by these changes. The importance of Section 1033 of the Dodd-Frank Act cannot be overstated, as it aims to foster an environment that encourages consumer empowerment and healthy competition among financial institutions. As the discourse around consumer financial protection evolves, striking the right balance between regulation and innovation will be crucial for the future of digital finance.

Applying for a merchant account is a crucial step for businesses looking to accept credit and debit card payments. The first step in the application process typically involves researching different payment processing providers to find one that aligns with your business needs. Consider factors such as transaction fees, customer service, and compatibility with your existing sales systems. Once you’ve selected a provider, you’ll need to complete an application form that generally requires basic information about your business, including your business structure, financial history, and processing volume. Depending on the provider, you may also need to submit documents like your business license, tax identification information, and bank statements to verify your legitimacy and ensure compliance with financial regulations.

After submitting your application, the payment processor will review your information and may conduct a background check or inquire about your transaction history. This process can take anywhere from a few hours to several days. Once approved, you’ll receive details about your account and how to integrate payment processing into your operations. It’s essential to read through all the terms and conditions before finalizing the agreement. For additional insights on the state of the payments industry and resources related to merchant accounts, visit the comprehensive overview available at Payments Dive: https://www.paymentsdive.com/news/cfpb-open-banking-comments-stripe-jpmorgan-mastercard-aba-fta-eta/803570/.

Understanding the Consumer Financial Protection Bureau (CFPB) and Its Role in Open Banking

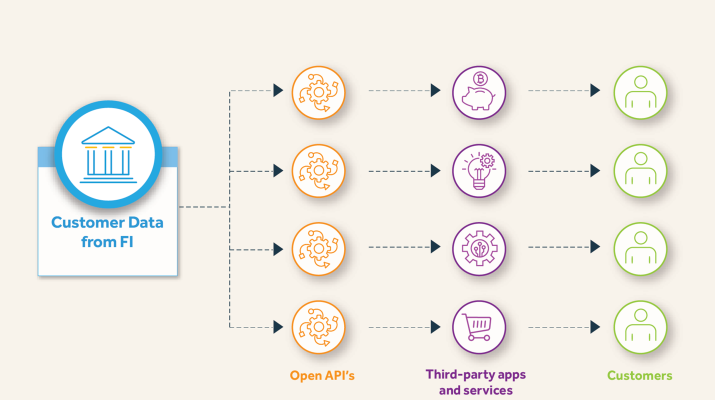

The Consumer Financial Protection Bureau (CFPB) plays a pivotal role in safeguarding consumers against exploitative practices and ensuring transparency in financial services. Established under the Dodd-Frank Act, the CFPB aims to regulate financial institutions and protect consumers’ rights in various financial matters, including lending, banking, and payment services. With the recent increased focus on open banking regulations, the CFPB is tasked with addressing complex interactions between traditional banks and fintech companies, ensuring that consumers retain control over their financial data while fostering competition in the market.

The CFPB is responsible for implementing regulations under Section 1033, which aims to facilitate open banking by allowing consumers to share their financial data securely with third-party providers. This initiative intends to empower customers and improve their financial decision-making capabilities by enabling them to choose better financial products and services. However, the CFPB’s efforts are not without controversy, as indicated by the significant pushback from banks, which argue that these regulations undermine their control and profitability. As the CFPB navigates these challenges, it must balance consumer protection with innovation in the financial technology sector.

The Impact of the Open Banking Rule on Financial Technology

The open banking rule, introduced last October, represents a significant shift towards greater access to consumer data within the financial services industry. At its core, this rule is designed to enhance competition among financial technology (fintech) providers, allowing them to tap into consumers’ bank data more readily. As technology continues to evolve rapidly, traditional banks face increasing pressure to innovate and adapt, as businesses like fintech sleekly offer tailored financial solutions based on consumer preferences and behaviors, ultimately benefiting the consumer.

As fintech regulations continue to evolve, stakeholders such as consumer advocates and regulatory bodies are keenly observing the implications of this rule. Comments from industry leaders, including firms like Stripe, indicate that these changes could dramatically influence payment processes, particularly concerning emerging technologies like stablecoins and AI in commerce. The open banking rule’s implementation is seen as vital for propelling further innovation in this sector, thus potentially transforming how consumers interact with financial services and enhancing the efficiency of financial transactions.

Stakeholders’ Perspectives on the Open Banking Rule

Numerous stakeholders across the financial spectrum have weighed in on the CFPB’s open banking rule, highlighting the diverse interests affected by the proposed changes. From fintech firms to traditional banks and consumer advocacy groups, the commentary reflects a growing concern regarding the implications of these regulations. Banks argue that the open banking framework could undermine their business models, incentivizing increased regulations that may stifle their competitive edge against agile fintechs eager to drive innovation.

Conversely, fintech firms and consumer advocates champion the open banking provisions, emphasizing the potential for improved financial accessibility and consumer choice. They argue that regulation under Section 1033 is essential for leveling the playing field, allowing smaller providers to compete against established banks. As the debate continues, it becomes increasingly clear that a collaborative approach involving multiple stakeholders is crucial for crafting regulations that both protect consumers and support fintech innovation in a rapidly changing environment.

Challenges Faced by the CFPB in Revising the Open Banking Rule

Revising the open banking rule presents numerous challenges for the CFPB, especially amidst a politically fragmented environment. With a Congress divided on financial sector regulations, the agency must be careful in its approach to ensure that the final rule reflects a broad consensus among diverse stakeholders. Recent comments from acting director Russell Vought hint at pending changes within the CFPB and its operation, raising concerns about the continuity of policies meant to bolster consumer protection amid a rapidly evolving fintech landscape.

Additionally, the legal battles stemming from banks’ lawsuits against the CFPB regarding overreach create further complexity. As courts navigate these challenges, the CFPB is tasked with considering stakeholder feedback while striving to maintain the integrity of the original intentions of open banking—to enhance competition and consumer choice. Achieving this balance is critical in establishing a regulatory framework that encourages innovation without sacrificing the consumer protections integral to the CFPB’s mission.

Future of Financial Services: The Role of Open Banking

The future of financial services is strongly tied to the successful implementation of open banking rules and regulations. By allowing consumers to easily share their financial data with multiple service providers, open banking has the potential to redefine how financial services are delivered. It paves the way for innovation by allowing fintech companies to offer personalized products that cater directly to individual needs, ultimately enabling consumers to make smarter financial choices.

However, for open banking to truly revolutionize the financial landscape, robust regulatory oversight is essential. As emerging technologies like blockchain, AI, and mobile payments become more integrated into everyday transactions, regulatory bodies like the CFPB must ensure that consumer interests remain protected while fostering an environment conducive to innovation. This delicate balance will determine the future trajectory of financial services, allowing for greater competition and accessibility.

Industry Reactions: Banks vs. Fintech in Open Banking Discussions

The ongoing discussions regarding the open banking rule have amplified the divisions between banks and fintech companies. Traditional banks have raised concerns about the potential implications of these regulations on their operations, arguing that they could disrupt longstanding business models and increase operational costs. Responding to the proposed rule changes, banks have mobilized their resources to voice opposition, claiming that the intended consumer benefits could be overshadowed by unforeseen challenges.

On the flip side, fintech companies view the open banking rule as a groundbreaking opportunity to expand their market presence. They argue that enabling consumers to control their financial data will drive innovation and facilitate the development of new financial products tailored to consumer needs. With industry leaders advocating fiercely for the open banking framework, the debate serves as a critical inflection point that could shape the future landscape of financial services and redefine the roles of banks and fintech companies alike.

Evaluating the Consumer Advocacy Perspective on Open Banking

Consumer advocacy groups play a crucial role in the dialogue surrounding the open banking rule, championing the importance of consumer rights and data protection. These organizations argue that by enabling consumers to manage their financial data, open banking enhances transparency and accountability within the financial services sector. Their advocacy emphasizes that consumers should have the ultimate control over their data and the ability to choose service providers, aligning with the consumer protection goals of the CFPB.

Moreover, consumer advocates are concerned about potential pitfalls associated with open banking, including data privacy and security risks. They continuously lobby for stringent regulations that ensure consumer data remains protected from misuse by both banks and fintech firms. As the CFPB moves forward with revising the rule, the input from consumer advocacy groups will be vital to shaping a regulatory framework that effectively addresses these concerns while promoting an innovative and consumer-friendly financial ecosystem.

The Legal Landscape Surrounding Open Banking and CFPB Regulations

The legal landscape surrounding open banking and the associated regulations by the CFPB presents a complex framework influenced by various stakeholders and ongoing litigation. Banks and other financial institutions have raised legal challenges to the CFPB’s authority to impose such sweeping regulations, arguing that it exceeds its jurisdiction. This has led to a contentious atmosphere, complicating the CFPB’s efforts to implement the open banking rule in alignment with Section 1033 of the Dodd-Frank Act.

As these legal battles unfold, the CFPB must navigate court decisions that may impact the future of open banking regulations. Industry participants, including fintech companies and consumer advocacy groups, are closely monitoring these developments. The outcome of these legal challenges will be critical in determining not only the viability of the open banking rule itself but also the broader trajectory of fintech regulations and their implications for consumers and the financial services sector at large.

Compliance Challenges Ahead for Financial Institutions and Open Banking

As the compliance deadlines for the open banking rule approach, financial institutions face significant challenges in adapting to the regulatory requirements set forth by the CFPB. Banks, especially smaller community banks, have raised concerns about their ability to meet the upcoming deadlines while ensuring that they maintain secure and compliant systems. The complexity of the regulations requires comprehensive changes to their operational frameworks, which could incur substantial costs and resource allocation.

Furthermore, as larger institutions lead the way in implementing changes, smaller banks and credit unions fear being left behind in the regulatory framework. The CFPB’s regulations under Section 1033 intend to foster competitiveness across the industry, but the compliance burden may disproportionately affect smaller institutions. As the open banking landscape evolves, collaborative solutions and clear guidance from regulators will be necessary to ensure that all financial institutions can adapt effectively without compromising consumer protections.

| Stakeholder | Position / Comments |

|---|---|

| Sen. Cynthia Lummis (R-WY) | Supports open banking, emphasizing it allows innovation and competition. |

| Apple | Advocates for maintaining open banking but excluding digital wallets from regulation as data providers. |

| Stripe | Cautions that CFPB decisions impact innovation in payments and AI commerce. |

| American Fintech Council & Others | Request for prohibition of data access fees and maintaining compliance deadlines. |

| JPMorgan Chase | Supports fees for data access to encourage secure practices and market valuation. |

| Mastercard | Generally supports the rule but seeks clearer data usage terms. |

| American Bankers Association (ABA) | Calls to suspend mid-2026 compliance deadlines and eliminate exemptions for smaller banks. |

| Retail Industry Leaders Association (RILA) | Warns against imposing data-access fees that harm competition. |

Summary

The open banking rule is a significant initiative aimed at enhancing competition in the financial services sector by allowing consumers greater control over their personal data. With various stakeholders expressing their views, there is a clear division between traditional banks and fintech companies on the implementation of this rule. The comments gathered by the CFPB indicate a strong desire for a balanced approach that fosters innovation while ensuring consumer protection. As the situation evolves, maintaining the integrity of the open banking rule will be crucial to advancing the interests of consumers and fostering a competitive landscape in the financial technology arena.

The open banking rule is reshaping the landscape of financial services, allowing consumers unprecedented control over their personal financial information. Recently, the Consumer Financial Protection Bureau (CFPB) received an overwhelming 14,000 public comments as it seeks to refine this pivotal regulation. This influx of feedback highlights the intense debate between traditional banks and fintech companies regarding data access and consumer rights. Key stakeholders, including consumer advocates and industry insiders, are examining how these fintech regulations, like Section 1033, can enhance or hinder innovation. As discussions unfold, the CFPB’s decisions will play a crucial role in the future of financial technology and the protection of consumer interests in a rapidly evolving marketplace.

The emerging framework surrounding consumer data sharing has become a focal point for discussions within the financial industry. Known colloquially as the financial data access policy, this rule aims to enhance competition among service providers by making it easier for consumers to choose and switch financial services. With insights coming from various sectors, including technology firms and advocacy groups, there is heightened scrutiny of the Consumer Financial Protection Bureau’s role in advancing these fintech guidelines. This initiative, particularly Section 1033, is critical in determining how consumers navigate and manage their financial information, which is increasingly becoming a valuable resource in today’s digital economy. As stakeholders weigh the implications of these regulations, they will have a lasting impact on the evolution of financial services and consumer rights.

Frequently Asked Questions

What is the Consumer Financial Protection Bureau’s (CFPB) role in the open banking rule?

The Consumer Financial Protection Bureau (CFPB) is responsible for overseeing financial regulations, including the open banking rule set forth in Section 1033 of the Dodd-Frank Act. This rule aims to empower consumers by allowing them to control their financial data and facilitate competition among financial service providers, including banks and fintech companies.

How does the open banking rule impact consumers and fintech companies?

The open banking rule enables consumers to easily share their financial data with new fintech companies, potentially offering them better financial services and products. This regulation promotes innovation in the financial technology sector, as fintech companies can develop applications that leverage consumer data to enhance financial management and services.

What are the main concerns surrounding the open banking rule according to banks?

Many banks are concerned that the open banking rule could lead to increased competition that undermines their market position. They argue that it may expose sensitive consumer data to risks and advocate for regulations that impose fees for data sharing to ensure that costs are covered while maintaining security.

What does Section 1033 of the Dodd-Frank Act entail regarding open banking?

Section 1033 of the Dodd-Frank Act mandates that financial institutions allow consumers to access and share their financial data with third-party providers. This section of the act is pivotal in advancing the objectives of the open banking rule, which aims to enhance consumer control over personal financial information.

How are comments from various stakeholders influencing the open banking rule revisions?

Feedback from diverse stakeholders, including fintech associations, banks, consumer advocates, and technology firms, is being considered by the CFPB in its revision process. This commentary is crucial in shaping a well-reasoned approach to the open banking rule that addresses various interests and maintains market integrity.

Why do some legislators support the open banking rule despite the opposition from banks?

Legislators like Senator Cynthia Lummis view the open banking rule as a vital element of financial innovation that enhances consumer rights. They argue that empowering consumers to control their financial data fosters competition and prevents large banks from stifling technological advancements in financial services.

What are the compliance timelines for the open banking rule set by the CFPB?

The CFPB has established compliance deadlines for the open banking rule, with the largest banks required to comply by July 1, 2026, while smaller banks will have phased compliance through 2030. Exemptions apply to financial institutions with less than $850 million in assets.

What is the potential impact of the CFPB’s decisions on the future of fintech?

The CFPB’s decisions on the open banking rule could significantly shape the evolution of the fintech landscape. A favorable regulatory environment could encourage innovation and the adoption of new technologies, while stringent rules or restrictions could hinder growth and drive fintech activities overseas.

How do payment processors view the open banking rule and its implications for payments?

Payment processors, like Stripe, believe the open banking rule will profoundly impact payment systems, affecting everything from the evolution of artificial intelligence in finance to the viability of digital currencies. They suggest that careful regulation is essential to avoid fees and limitations that could stifle innovation.

What are the arguments against imposing fees for accessing consumer financial data under the open banking rule?

Critics argue that imposing data-access fees under the open banking rule would create barriers to entry for fintechs and diminish competition. They believe that consumer access to their financial data should be free to encourage innovation and prevent large financial institutions from monopolizing access.

The Consumer Financial Protection Bureau (CFPB) plays a pivotal role in regulating financial technology (fintech) companies, which have been rapidly evolving in the landscape of consumer finance. As a governmental agency established to protect consumer interests in the financial sector, the CFPB addresses various aspects of fintech operations, ensuring they adhere to laws designed to safeguard consumer rights. This includes monitoring practices related to transparency, fair lending, and data privacy, which are critical components in the digital finance arena. The increasing complexity and diversity of fintech solutions necessitate close scrutiny by the CFPB to mitigate risks posed to consumers.

Fintech regulations have become increasingly relevant as technology continues to reshape how financial services are delivered. The CFPB is at the forefront of implementing these regulations, helping to ensure that innovations such as mobile payments, peer-to-peer lending, and robo-advisors operate within a safe and regulated framework. By establishing guidelines, the CFPB aims to protect consumers from potential abuses while still fostering an environment where technology can improve access and convenience in financial transactions. These regulations must strike a balance between innovation and consumer protection, encouraging responsible growth in the fintech sector.

Section 1033 of the Dodd-Frank Act is particularly significant in the context of fintech regulations. It grants consumers the right to access their financial information held by financial institutions, thereby fostering transparency and empowering consumers to make informed decisions regarding their finances. This section is crucial for fintech companies that rely on consumer data to provide personalized services and products. The CFPB’s work in implementing Section 1033 ensures that consumers’ financial data is accessible and transferable, enhancing competition among fintech services and preventing monopolistic practices in the rapidly evolving digital finance space.

The recent commentary collected by the Consumer Financial Protection Bureau (CFPB) on its open banking rule highlights the diverse interests involved in the ongoing debate surrounding consumer financial data access. With over 14,000 comments, stakeholders from various sectors, including banks, fintech companies, advertisers, and consumer advocates, are expressing their views on how to navigate the complexities of personal financial information control. As the CFPB works to revise the open banking rule, which is designed to enhance competition among financial service providers by allowing consumers to share their data more freely, the tension between traditional financial institutions and emerging fintech players remains a central theme.

Senator Cynthia Lummis praised the Section 1033 open banking provision of the Dodd-Frank Act as a crucial advancement for digital finance. She cautioned against allowing established financial entities to obstruct innovation in favor of their interests, suggesting that doing so would push entrepreneurial efforts abroad and diminish the United States’ standing in financial technology. This sentiment echoes concerns from various fintech representatives who argue that imposing additional barriers, like data access fees or complex compliance requirements, could stifle the industry’s potential and limit the benefits intended for consumers.

Amidst this backdrop, the CFPB’s leadership transition, marked by acting director Russell Vought’s remarks about the agency’s potential downsizing, raises questions about the future enforcement of the open banking rule. Despite the uncertainty surrounding the CFPB’s operations, fintech advocates emphasize that existing regulations remain enforceable. They urge the agency to adhere to its initial intentions of promoting transparency and competition in financial services, insisting that any revisions should not compromise consumer rights or the progress already made.

The diverse opinions collected in the comment period underscore the complexity of achieving a balanced open banking framework. For instance, major corporations like Apple and payment processors like Stripe highlight the necessity of defining data responsibilities and prohibiting excessive fees that could obstruct innovation. The call for a collaborative discussion among industry stakeholders, as suggested by the Electronic Transactions Association, reflects a recognition of the need for constructive dialogue to address operational implications while striving for a consensus that can support a fair and dynamic financial service landscape.

Financial giants, including JPMorgan Chase, have articulated distinct positions by proposing adjustments to the current rule, such as introducing fees for data access, while facing backlash from fintech firms advocating for continued free access. The Retail Industry Leaders Association echoes similar frustrations, warning against a potential retention of interchange fees that could mirror previous inefficiencies in the payment processing sector. These perspectives expose the broader challenge of striking a balance where both innovation and consumer protections are prioritized in the rapidly evolving financial ecosystem.