Navigating the complexities of business financing can be daunting, but getting a Capital One business credit card pre-approval is a strategic step that can empower your entrepreneurial journey. This crucial process not only helps to determine your credit card eligibility without affecting your credit score but also presents an opportunity to strategize your business credit effectively. With insights on business credit card tips and essential documentation, you’ll be better equipped to tackle the pre-approval process. Moreover, understanding Capital One’s offerings can maximize your benefits, from cashback incentives to no annual fees, enhancing your overall business credit strategy. Start today and unlock the potential that a Capital One business credit card can provide for your growth.

In the realm of small business financing, the pathway to securing a credit line often begins with exploring options like Capital One’s business card pre-qualification. This preliminary stage, which allows prospective applicants to gauge their chances of approval, facilitates a smoother transition into obtaining credit without negatively impacting credit scores. Understanding the nuances of creditworthiness and taking note of valuable insights on various business cards can help in making informed financial decisions. Additionally, aligning your financial profile with the eligibility criteria not only prepares you for potential acceptance but also optimizes your ability to leverage credit as a powerful asset for future successes. From analyzing rewards to understanding interest rates, the pre-qualification process is a vital first step in establishing solid business financial strategies.

Applying for a merchant account is a critical step for businesses looking to accept credit and debit card payments from customers. The first step in the application process is to select a reputable payment processor that suits your business needs. Research various providers, comparing their fees, services, and features to find the best fit. Once you’ve chosen a provider, visit their website and fill out the online application form, which typically requires information about your business, such as the type of products or services offered, monthly sales volume, and bank account details. Be prepared to provide documentation such as your business license, tax ID number, and proof of identity as part of the verification process.

After submitting your application, the payment processor will review it to assess the risk involved with providing your business a merchant account. This may include a credit check or background checks on your business and its owners. The entire process can take anywhere from a few hours to a few days, depending on the provider’s internal procedures. Once approved, you will receive your account details, and you’ll be able to set up the necessary payment processing hardware or software. If you need assistance or have questions during the application process, most payment processors offer customer support resources and guides on their websites to help streamline your experience.

Unpacking the Pre-Approval Process for Capital One Business Credit Cards

Understanding the pre-approval process for a Capital One business credit card is essential for any entrepreneur looking to leverage credit as a financial tool. Pre-approval allows you to gauge your eligibility without causing harm to your credit score, as it involves a soft inquiry rather than a hard one. This means that you can explore your options with the added advantage of knowing where you stand financially before making a formal application. In today’s fast-paced business environment, being proactive about credit management is a critical aspect of financial strategy.

Taking the time to comprehend this process can significantly enhance your chances of securing the credit card that best suits your business needs. By getting pre-approved, you gain access to valuable insights about your financial standing and can make informed choices regarding your credit options. A pre-approval outcome not only equips you with tailored suggestions from Capital One but also reinforces your negotiation position when seeking the best available terms and rewards.

Essential Eligibility Criteria for Capital One Business Credit Card

Before applying, it is vital to understand the eligibility criteria that Capital One uses to evaluate business credit applications. Key factors include your credit score, which generally requires a minimum of 650 for approval. A higher credit score indicates better financial responsibility and payment history, elements that are critical for lenders. Alongside credit score, aspects such as your business’s financial management practices, like maintaining a low credit utilization ratio and meeting debt obligations on time, can significantly boost your approval odds.

It’s also important to demonstrate a clear separation between personal and business finances. This distinction not only strengthens your business creditworthiness but also enhances your eligibility for other business credit products. Gathering and presenting your financial documentation accurately, including your Employer Identification Number (EIN) and recent financial statements, will set the stage for a successful pre-approval process.

Maximizing Your Approval Chances: Documentation and Best Practices

Proper documentation can make all the difference when applying for a Capital One business credit card. Key documents include your Employer Identification Number (EIN) and business tax ID, which are fundamental for establishing your business’s identity. Additionally, providing clear and organized financial statements, such as revenue projections and historical profit or loss figures, can convincingly demonstrate your business’s financial health. This level of preparedness signals to Capital One that you are a responsible borrower and enhances your profile in the pre-approval process.

To further bolster your application, consider best practices such as regularly monitoring your credit score prior to your application and addressing any discrepancies. Additionally, reducing existing credit card balances will lower your credit utilization ratio, a crucial factor that credit issuers look for. By showing that your current debts are manageable, you stand a better chance of receiving favorable terms and conditions from Capital One.

Benefits of Exploring Multiple Credit Card Options for Your Business

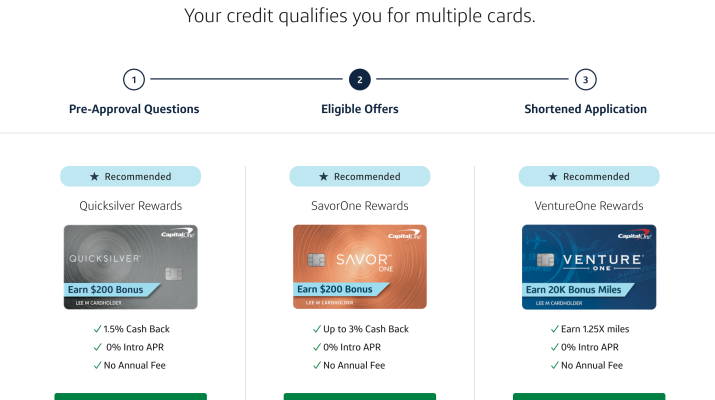

While a Capital One business credit card might be an excellent choice, exploring multiple credit options can provide you with a broader perspective on the best financial products available. Different banks and financial institutions offer unique benefits such as varied rewards programs, interest rates, and annual fees. By comparing these variables across various cards, you can make a more informed decision that aligns with your business’s specific expenditures and future goals.

For instance, if your business frequently incurs travel expenses, you might find a card that offers enhanced travel rewards or points more suitable than a general cashback card from Capital One. Additionally, reviewing aspects such as APR can help you avoid high-interest charges, ensuring financial sustainability. Ultimately, an informed comparison can lead to a smarter credit strategy that benefits your business’s financial health.

| Key Points | Details |

|---|---|

| Understanding Pre-Approval | Pre-approval allows applicants to assess eligibility without affecting their credit score. |

| Benefits of Pre-Approval | 1. Helps assess risk. 2. Informs better credit card decisions. |

| Eligibility Criteria | 1. Good credit score (650+). 2. Maintain healthy financial management between personal and business finances. |

| Documentation Required | 1. Employer Identification Number (EIN). 2. Business Tax ID. 3. Financial Statements. |

| Using the Capital One Website | Navigate to the business credit section, fill out the application, and review card options. |

| Explore Multiple Options | Consider rewards programs, interest rates, and annual fees offered by various cards. |

| Reducing the Risk of Rejection | 1. Pay down credit card balances. 2. Consolidate debts. 3. Check your credit score regularly. |

| Additional Resources | Refer to Capital One and financial advice blogs for up-to-date information. |

Summary

Capital One business credit card pre-approval is an essential step for entrepreneurs seeking to secure financing for growth and operations. Understanding the pre-approval process allows business owners to evaluate their eligibility without affecting their credit scores. By meeting the eligibility criteria, gathering the necessary documentation, and minimizing risks of rejection, applicants can enhance their chances of approval. Furthermore, exploring various credit offerings ensures that businesses select cards that align with their financial needs. Overall, initiating the Capital One pre-approval process can set the stage for effective credit management and business success.

Frequently Asked Questions

What is the Capital One business credit card pre-approval process?

The Capital One business credit card pre-approval process involves a soft credit inquiry to assess your eligibility without impacting your credit score. You’ll fill out an online application, providing details about your business and personal finances, and Capital One will evaluate your creditworthiness before offering pre-approval for specific card options.

What are the eligibility criteria for Capital One business credit card pre-approval?

To qualify for Capital One business credit card pre-approval, you generally need a good credit score (around 650 or higher), a strong financial management record, and necessary documentation like your Employer Identification Number (EIN) and financial statements. This will help demonstrate your business’s financial stability.

How can I improve my chances of Capital One business credit card pre-approval?

To boost your chances of Capital One business credit card pre-approval, consider reducing existing credit card balances, consolidating debts, and regularly checking your credit score for accuracy. Maintaining a low credit utilization ratio and ensuring timely payments on debts can enhance your creditworthiness and support a successful application.

What documents do I need for Capital One business credit card pre-approval?

For Capital One business credit card pre-approval, be prepared to provide your Employer Identification Number (EIN), business tax ID, and relevant financial statements such as revenue figures and profit/loss statements. These documents substantiate your business’s financial health and improve your approval prospects.

When it comes to managing business expenses, having a business credit card can be a game-changer for entrepreneurs. One of the top tips for utilizing business credit cards effectively is to ensure timely payment to build and maintain a strong credit score. This means paying off the full balance each month to avoid interest accrual. Additionally, it is wise to segregate personal and business expenses, making bookkeeping easier and enhancing the credibility of financial records. Lastly, choosing a card with rewards that align with your business spending can yield significant benefits, such as cashback or travel points.

Capital One offers a variety of credit cards tailored to different business needs, including options with no annual fees and those providing robust cash-back rewards. Business owners should explore options like the Capital One Spark Cash for Business, which gives unlimited 2% cash back on every purchase, or the Capital One Spark Miles for Business, which offers 2 miles per dollar on every purchase. These cards not only help in managing day-to-day expenses but also provide a way to earn rewards that can be reinvested into the business or redeemed for personal use.

Before applying for a business credit card, understanding eligibility is crucial. Generally, issuers require business owners to have a valid Employer Identification Number (EIN) or Social Security number for sole proprietors. Other factors considered include the credit score of the business owner, the business’s revenue, and time in operation. Being aware of these criteria can help ensure you apply for a card that aligns with your financial profile and increases the likelihood of approval.

The pre-approval process for a business credit card is designed to help entrepreneurs gauge their eligibility without affecting their credit score. By submitting basic business information and financial projections, small business owners can receive a soft inquiry from the lender, which helps them understand their chances of securing the desired card. This step is beneficial as it allows for comparisons between different cards and terms while maintaining a strong credit standing.

Developing a solid business credit strategy involves more than just obtaining a credit card; it includes a comprehensive approach to managing finances. Entrepreneurs should focus on building a separate credit profile for their business, which involves regularly using business credit cards, repaying debts on time, and actively monitoring credit scores. Additionally, utilizing credit responsibly can enhance borrowing power for business expansions or cash flow needs down the line. Strategic financial management and leveraging credit effectively can pave the way for sustained growth and success.

Navigating the world of business credit can be daunting, especially for new entrepreneurs. One crucial step in securing essential funding is getting pre-approved for a Capital One business credit card. This process allows you to gauge your eligibility without putting your credit score at risk, giving you a clear picture of your options. Before diving into the application, it’s important to understand pre-approval’s benefits, which include knowing your potential credit limit and card features that best fit your business needs. This understanding can help streamline your financial strategy and prepare for future investments.

To increase your chances of a successful pre-approval, focus on understanding the eligibility criteria laid out by Capital One. A good credit score, typically around 650 or higher, is fundamental. Beyond your personal credit score, demonstrating sound financial management of your business is vital. Monitor your credit utilization ratio and ensure timely repayment of any existing debts. These steps not only establish your creditworthiness but also reflect responsible financial behavior that lenders appreciate, making you a more attractive candidate for a business credit card.

Preparation is key when approaching the pre-approval process. Collect necessary documentation like your Employer Identification Number (EIN), business tax ID, and financial statements showcasing your business’s revenue and profit margins. Having this information ready allows for a smooth application process and ensures that you can provide accurate details, which increases your credibility with lenders. This proactive approach not only speeds up the process but also gives you an edge in presenting your business as a low-risk investment.

Utilizing Capital One’s official website effectively can significantly enhance your pre-approval experience. By navigating to the Business Credit section, you can easily find the application form and start providing the required information. Post-application, take the time to review all card options presented to you. Look for not just the interest rates but also the rewards and benefits associated with each card. Capital One often offers enticing cash back deals or travel rewards, which can add significant value to your business expenditures.

While focusing on a Capital One business credit card is essential, it’s beneficial to explore additional options across multiple financial institutions. Different credit cards provide unique rewards programs suited for diverse spending habits, which can better fit your business needs. Compare interest rates and annual fees among various cards to find the most advantageous terms. This comparison empowers you to make an informed decision that aligns not only with your current financial situation but also with your long-term business goals.

To minimize the risks of rejection, timing your application with your business’s financial health in mind can make a difference. Pay down existing credit card debts, as lower balances improve your credit utilization ratio, positively affecting your credit score. If you have multiple debts, consider consolidating them to simplify your payments. Regularly checking your credit score allows you to pinpoint areas for improvement, ensuring you’re in the best shape possible before initiating your pre-approval application. This preparation is crucial for maximizing your chances of approval.

Finally, taking advantage of additional resources can provide valuable insights as you embark on the pre-approval journey. Relying on Capital One’s website ensures you have the most current information regarding requirements and procedures. Financial advice blogs such as NerdWallet or The Points Guy can also provide tips on maximizing your credit card benefits and navigating the market effectively. By leveraging these resources, you equip yourself with knowledge that is essential for making strategic financial decisions.

In conclusion, pursuing pre-approval for a Capital One business credit card is a strategic step towards enhancing your business’s financial flexibility. By understanding the pre-approval process, meeting eligibility criteria, and preparing the necessary documentation, you can significantly increase your chances of obtaining approval. Additionally, exploring multiple credit card options ensures you select the best fit for your business strategy. By following these tips and strategies, you set the foundation for a successful path in leveraging credit as an asset for your business growth.