In today’s digital economy, credit card processing plays a pivotal role in enhancing payment solutions for small businesses. As cashless transactions become increasingly popular, mastering credit card processing is essential for merchants looking to thrive in a competitive marketplace. This guide delves into the intricacies of payment processing for small businesses, covering key topics like credit card transaction security and emerging online payment trends. Understanding how to choose a payment processor can significantly impact a small business’s efficiency and customer satisfaction. With a focus on seamless operations and robust security measures, small business payment solutions are more important than ever.

Credit card payment systems, often referred to as transaction processing, constitute a fundamental element of modern business operations. These systems not only facilitate payments but also empower small businesses to adapt to the rising tide of cashless transactions. Exploring various small business payment options, such as mobile payments and fraud prevention methods, is crucial in choosing an effective payment service. As online shopping continues to grow, understanding credit card transactions and security compliance ensures that merchants can confidently meet customer expectations. The evolution of online payment methods necessitates an informed approach to selecting the right transaction partner for sustainable business success.

Applying for a merchant account is a crucial step for any business looking to accept credit card payments and manage transactions smoothly. To begin the application process, you will first need to research and choose a merchant service provider that aligns with your business needs. Factors to consider include transaction fees, monthly costs, customer support, and the types of payment methods they accept. Once you’ve selected a provider, visit their website to find the application form, which may be available online or require you to contact their sales team directly. You will typically need to provide basic information about your business, such as its legal structure, annual revenues, and volume of credit card transactions you expect to process.

After you have submitted your application, the merchant service provider will review your information and assess your risk level. This process may take anywhere from a few hours to a couple of days, depending on their practices. Be prepared to provide additional documents, such as a copy of your business license, ID verification, and banking information if requested. Once approved, you will receive your merchant account details along with instructions on how to integrate the payment gateway or point of sale system into your business operations. For more comprehensive guidance on applying for a merchant account, you can visit [insert website or resource link here], where you’ll find step-by-step instructions and helpful tips to get started.

The Importance of Credit Card Processing for Small Businesses

Effective credit card processing is no longer optional for small businesses that wish to meet consumer expectations in the digital era. As shopping trends shift increasingly toward online and cashless transactions, merchants need processing solutions that ensure security and convenience. Implementing a robust credit card processing system can enhance customer satisfaction and drive sales, making acceptance of credit cards a foundational element of modern retail.

Moreover, with consumers favoring speed and efficiency, businesses that can facilitate quick, secure transactions will likely see improved customer loyalty. In an age where digital interactions dominate, optimizing credit card processing can serve as a powerful competitive advantage, helping businesses not only reach but exceed customer service expectations.

Understanding Credit Card Transaction Security

As online transactions become more prevalent, the security of credit card processing systems has taken center stage. Small business owners must understand the various security measures involved in payment processing to protect their customers’ data and maintain trust. Key security features include end-to-end encryption and compliance with the Payment Card Industry Data Security Standard (PCI DSS), which outlines a framework for protecting sensitive credit card information.

Additionally, businesses should stay abreast of cybersecurity threats and invest in technologies that bolster their defenses. Tools like two-factor authentication (2FA) provide extra layers of security and can considerably reduce the risk of data breaches. By prioritizing security in credit card processing, businesses can build a reliable reputation that fosters long-lasting customer relationships.

Emerging Online Payment Trends for Small Businesses

The landscape of online payment solutions is evolving rapidly, influenced by technological advancements and changing consumer preferences. Today, small businesses are witnessing an uptick in the adoption of mobile wallets and contactless payments. Consumers now expect the ability to make purchases seamlessly via their smartphones, reflecting a significant shift towards a more convenient and efficient payment experience.

For instance, incorporating mobile payment options like Apple Pay and Google Pay into the checkout process can attract tech-savvy customers and speed up transaction times. This trend underscores the necessity for small businesses to remain adaptable by embracing innovative payment methods that enhance customer convenience and streamline operational efficiencies.

Choosing a Payment Processor: Essential Considerations

The decision-making process in selecting a payment processor can be intricate yet pivotal for small businesses. Key factors to consider include transaction fees, which vary between flat-rate and interchange-plus pricing models. Understanding the nuances of these fees is essential, as they can impact profitability significantly. A thorough analysis of average transaction volumes can aid business owners in selecting a processor that aligns with their budget and financial goals.

Additionally, the level of customer support provided by the payment processor should not be overlooked. Responsive and knowledgeable support can make a significant difference during setup and ongoing operations, ensuring that issues are resolved promptly. Business owners should prioritize processors with transparent practices and a strong reputation for customer service, as this can relieve some of the operational burdens associated with payment processing.

Navigating Cost Considerations in Credit Card Processing

Understanding the various costs associated with credit card processing is crucial for small businesses looking to maintain healthy profit margins. Fees can include transaction fees, monthly service charges, and equipment costs, all of which can vary widely among processors. For instance, while flat-rate fees provide simplicity, they may not be the most economical choice for businesses with high sales volumes.

Conversely, an interchange-plus pricing model might offer better savings over time but requires more careful monitoring of transactions. Small business owners should regularly evaluate their payment processing costs and consider negotiating terms with their processors to ensure they are receiving the best rates available.

Innovative Technology Impacting Payment Systems

As technology continues to advance, small businesses must keep pace with emerging innovations in the payment processing landscape. New developments such as artificial intelligence and machine learning are enhancing fraud detection capabilities, which in turn improve transaction security. Moreover, blockchain technology is being explored for its potential to streamline payment processing through decentralized ledgers, offering an additional layer of transparency and security.

Additionally, the growth of ‘buy now, pay later’ services is rapidly changing payment preferences among consumers. By integrating such innovative solutions, small businesses can cater to evolving customer expectations and gain a competitive edge in an increasingly crowded marketplace.

The Role of Customer Experience in Payment Processing

The customer experience during the payment process can significantly influence consumer satisfaction and, ultimately, the success of a small business. A simplified checkout experience, which may include features like saved payment information or a variety of payment options, can lead to higher conversion rates. When consumers encounter seamless transactions, they are less likely to abandon their carts and more inclined to return for future purchases.

Furthermore, businesses that proactively seek customer feedback regarding their payment systems can uncover critical insights for improvement. By focusing on enhancing the overall payment experience, small businesses can drive customer loyalty and foster long-term relationships, which are essential for growth in today’s competitive landscape.

Preparing for Future Changes in Payment Processing

As the financial landscape continues to evolve, it’s essential for small businesses to stay informed about future trends in payment processing. Legislative changes, technological advancements, and shifts in consumer behavior are all factors that could reshape how credit card transactions are handled. By remaining adaptable and open to new ideas, businesses can position themselves to take advantage of these changes and maintain relevancy in their markets.

Anticipating these shifts means investing in continuous education about payment technologies and security practices. By embracing a proactive approach to adapting their payment methods and infrastructures, small businesses not only safeguard themselves against potential disruptions but also ensure they remain appealing to their target audience.

The Future of Credit Card Processing in Small Business

The future of credit card processing holds immense potential for small businesses as automation and advanced technology pave the way for more efficient transactions. Additionally, the rise of artificial intelligence in payment systems is expected to enhance fraud detection and streamline operations, reducing the burden on business owners. Adopting these innovations will not only protect business interests but also improve overall customer experience.

Furthermore, as consumers demand even more convenience, future credit card processing solutions could include biometric verification methods, such as facial recognition or fingerprint scanning, ensuring secure transactions while enhancing speed. By keeping an eye on such advancements and integrating them strategically, small businesses can remain competitive and cater to the ever-changing preferences of their customers.

| Key Components of Credit Card Processing | Current Trends | Choosing a Payment Processor | Security and Compliance | Emerging Technologies | Cost Considerations | Enhancing Customer Experience |

|---|---|---|---|---|---|---|

| Authorization, Capture, Settlement are core phases. | Shift to digital payments post-pandemic; need for integrated systems. | Consider transaction fees, setup costs, and customer support. | Compliance with PCI DSS is crucial; invest in security measures. | Increased use of contactless payments and blockchain technology. | Analyze transaction volumes to select the best fee structure. | Smooth payment process enhances customer satisfaction and loyalty. |

Summary

Credit Card Processing has emerged as a vital aspect for small businesses aiming to stay competitive in today’s market. Initially, small business owners need to comprehend the core processes involved—authorization, capture, and settlement—ensuring they manage transactions effectively. Following this, they should adapt to the evolving trends that have gained traction in the wake of the pandemic, highlighting the importance of digital payment solutions. The selection of an appropriate payment processor comes next, where factors like fees, costs, and customer support guide informed choices. Security remains paramount; adhering to PCI compliance and implementing protective measures is essential for safeguarding customer data. As new technologies such as contactless payments and blockchain advancements arise, businesses can enhance their operations, leading to an improved customer experience. Finally, a thorough understanding of cost considerations aids in maintaining profitability. Thus, as the digital era of transactions unfolds, grasping the nuances of credit card processing will undeniably empower small businesses to flourish.

Frequently Asked Questions

What is the process of credit card processing for small businesses?

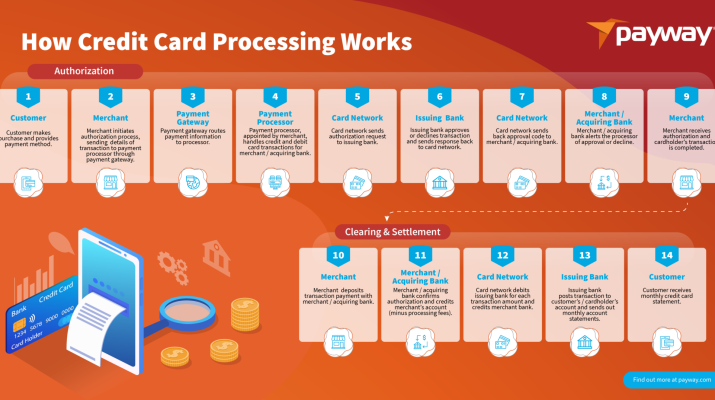

Credit card processing for small businesses involves three main phases: authorization, capture, and settlement. Authorization verifies the customer’s card details with the payment processor. Capture securely records the transaction, and settlement transfers the funds from the customer’s bank to the merchant’s account.

How can small businesses choose the right payment processor?

When choosing a payment processor, small businesses should consider factors such as transaction fees (flat-rate vs. interchange-plus), setup costs, and customer support. Popular options like Square, PayPal, and Stripe are user-friendly and well-suited for small business needs.

What are some current trends in credit card processing?

Current trends in credit card processing include the rise of contactless payments and the integration of point of sale (POS) systems for both online and offline sales. Businesses must adapt to these trends to meet consumer demands for flexibility and convenience.

What security measures should small businesses implement for credit card processing?

Small businesses must comply with PCI DSS standards to ensure credit card transaction security. Implementing end-to-end encryption and two-factor authentication can help protect cardholder data and prevent fraud.

What cost considerations should small businesses keep in mind regarding credit card processing?

Cost considerations in credit card processing include transaction fees that can vary significantly. Small businesses should analyze their transaction patterns and fee structures to choose a processor that minimizes costs while maximizing efficiency.

What is the importance of customer experience in credit card processing?

A streamlined credit card processing system enhances customer experience, leading to increased satisfaction and loyalty. Offering various payment options and a smooth checkout process can significantly boost sales for small businesses.

How are emerging technologies influencing credit card processing?

Emerging technologies like mobile wallets (Apple Pay, Google Pay) and blockchain are reshaping credit card processing. These innovations improve transaction speed and security, which can enhance the overall customer experience.

What is the significance of compliance in credit card processing security?

Compliance with PCI DSS is critical for credit card processing security. It sets strict guidelines for handling cardholder data safely and helps mitigate the risks of fraud and data breaches for small businesses.

How do transaction fees affect small business payment solutions?

Transaction fees directly impact the bottom line of small business payment solutions. Understanding the different fee structures can help owners choose the most cost-effective processor and improve overall profitability.

What online payment trends should small businesses be aware of?

Small businesses should be aware of trends such as increased consumer preference for cashless payments, the growth of e-commerce, and the adoption of advanced payment technologies like contactless and peer-to-peer payment systems.

Payment processing for small businesses is an essential component of operational efficiency and customer satisfaction. Small businesses often face unique challenges compared to larger enterprises, such as limited resources and expertise. An effective payment processing solution can help streamline transactions, improve cash flow, and enhance the customer experience. With various options available, from traditional point-of-sale systems to mobile payment solutions, small businesses can choose the tools that best suit their needs.

Choosing a payment processor involves careful consideration of several factors, including transaction fees, integration capabilities, and customer support. Small businesses should evaluate processors based on their specific industry and clientele. For example, a retail shop may prioritize face-to-face transaction capabilities, while an e-commerce business might need a robust online payment system. Additionally, understanding the fee structures and potential hidden costs is crucial to avoid unexpected expenses.

Credit card transaction security is more important than ever in today’s digital age. Small businesses must protect sensitive customer information to maintain trust and compliance with regulations such as the Payment Card Industry Data Security Standard (PCI DSS). Businesses should utilize secure payment gateways, implement encryption technologies, and regularly update their security measures to safeguard against data breaches and cyber attacks. Ensuring a secure transaction environment is essential not only for legal compliance but also for maintaining customer loyalty.

Online payment trends are constantly evolving, influenced by technological advancements and changing consumer preferences. Currently, mobile wallets, contactless payments, and buy now, pay later (BNPL) solutions are gaining traction among consumers, particularly among younger demographics. Small businesses that adapt to these trends can enhance their customer experience and potentially increase sales volume. Staying informed about these trends allows businesses to remain competitive and responsive to their customers’ needs.

Small business payment solutions have diversified significantly, providing various options tailored to different operational sizes and needs. From traditional merchant accounts to modern integrated payment platforms, small businesses can now select solutions that not only facilitate transactions but also offer additional features like inventory management, sales reporting, and customer relationship management. Effective payment solutions can help small businesses save time, reduce errors, and ultimately improve overall business performance.

In today’s market, small businesses face a myriad of challenges, and credit card processing stands out as a pivotal aspect of their operation. The journey of a credit card transaction begins when a customer decides to make a purchase. Once the customer presents their card, the payment processor springs into action, verifying the card’s authenticity and ensuring that there are sufficient funds in the customer’s account. This seamless interaction occurs behind the scenes and is crucial for both customer satisfaction and the business’s cash flow. Understanding these processes is paramount for small business owners, enabling them to troubleshoot potential issues and maintain high service standards.

The evolution of consumer payment preferences has led to notable trends in credit card processing. Small businesses are no longer merely accommodating traditional payment methods; they are now compelled to adapt to the rapid rise of e-commerce and contactless payments. With a growing number of consumers favoring online shopping and mobile transactions, businesses that invest in integrated POS systems and online payment gateways will not only meet customer demands but also enhance their operational efficiencies. As these trends continue to gain traction, keeping up with technological advancements in payment processing becomes increasingly essential.

When selecting a payment processor, small business owners must navigate an array of choices and considerations. One of the foremost factors to look at is the fee structure, as transaction costs can eat into profit margins significantly. Businesses should weigh the pros and cons of flat-rate fees against the interchange-plus rates. Additionally, initial setup costs and the quality of customer support should not be overlooked. A responsive payment processor can make a world of difference when technical issues arise, impacting the overall customer experience.

Ensuring the security of payment processing is crucial for small businesses, especially in an era where data breaches are increasingly prevalent. Compliance with PCI DSS is essential, providing a framework to protect sensitive customer information. Beyond compliance, implementing advanced security measures such as end-to-end encryption and tokenization can enhance the safety of transactions, further assuring customers that their financial data is secure. By prioritizing robust security practices, businesses not only protect themselves from fraud but also cultivate a trustworthy brand image.

The impact of emerging technologies on credit card processing cannot be understated. Innovations like mobile wallets and contactless payments are redefining how consumers interact with merchants. These technologies streamline the transaction process, providing a faster and more efficient checkout experience that enhances customer satisfaction. Furthermore, with the advent of blockchain technology, businesses can look forward to even greater levels of security and transparency in transactions. Embracing these technologies positions small businesses at the forefront of payment processing evolution.

As small business owners delve deeper into understanding credit card processing costs, it becomes clear that having a comprehensive awareness of transaction fees is vital for maintaining profitability. Different processors may have varying fees based on the type of transactions and volumes a business handles. To ensure cost-effectiveness, it is beneficial for businesses to analyze their transaction patterns and choose a processor that aligns with their specific needs, thereby minimizing unnecessary costs and maximizing operational efficiency.

A smooth payment processing system can significantly enhance the overall customer experience. When businesses provide diverse payment options and ensure a swift checkout process, they are more likely to foster customer loyalty. Satisfied customers often return, appreciate the convenience offered, and recommend the business to peers. Thus, investing in an efficient payment processing system is not merely an operational necessity; it serves as a strategic move to bolster customer satisfaction and retention.

In conclusion, navigated adeptly, credit card processing can become a powerful tool for small businesses in the digital age. By effectively analyzing transaction fees, ensuring security compliance, and staying updated with emerging technologies, small business owners can not only streamline their operations but also enhance customer satisfaction. The transition to a fully digital transaction landscape is not a challenge to fear but an opportunity to seize. By prioritizing credit card processing as a key business element, small enterprises can position themselves for growth and success in an increasingly competitive marketplace.