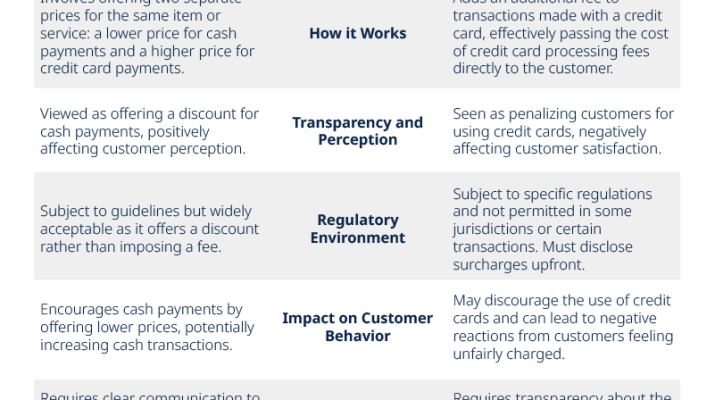

In today’s competitive marketplace, **dual pricing** has emerged as a powerful strategy for business owners aiming to maximize profits while minimizing expenses. This innovative approach allows establishments to charge varying prices depending on the payment method, providing a significant advantage against the rising **credit card fees** that burden many enterprises. With dual pricing, businesses can incentivize cash payments, ultimately striving for the sought-after goal of 0% credit card processing fees. This article will delve into the mechanics of dual pricing, discussing its benefits, potential challenges, and the latest industry trends to help you enhance your overall business pricing strategies. By understanding and implementing this dual pricing model, you can significantly improve your cash flow and retain more revenue.

Often referred to as differentiated pricing, the concept of **dual pricing** enables businesses to adopt varied pricing models based on the method of payment. This strategy not only combats the rising costs associated with credit transactions but also fosters an environment that encourages cash payments through appealing incentives. As consumer preferences shift and businesses seek ways to manage operational costs, alternative pricing strategies like dual pricing are becoming increasingly relevant. By embracing this approach, companies can strengthen their profit margins and ensure transparency for customers, ultimately shaping a more efficient and effective financial framework. The growing acceptance of cash incentives reflects a broader trend towards reevaluating traditional pricing methods in light of today’s economic challenges.

Applying for a merchant account is an essential step for businesses looking to accept credit and debit card payments. To begin the process, you should first research various merchant service providers to find one that aligns with your business needs. Key considerations include transaction fees, customer support, and the variety of payment methods each provider supports. Once you’ve selected a provider, you’ll typically need to fill out an application that includes your business details, banking information, and possibly a credit check. Be prepared to provide documentation such as your business license, tax ID, and financial statements to demonstrate your business’s stability and legitimacy.

After submitting your application, the merchant service provider will review your information and may ask for additional details or proof of identity. It’s crucial to promptly respond to any requests to expedite the approval process. Once approved, you’ll receive a merchant account and can start processing payments. Additionally, many providers offer integrated solutions with e-commerce platforms, allowing for seamless transactions online. For more information on specific steps and comparisons of various providers, consider visiting reliable financial service websites or industry blogs that outline the best options available for merchant accounts.

Understanding the Financial Impact of Dual Pricing

Dual pricing has emerged as a transformative pricing strategy for businesses seeking to mitigate the burdens of credit card processing fees. By implementing this model, companies can charge different prices depending on the payment method, effectively reducing the cost associated with credit card transactions. This approach not only alleviates the financial strain caused by processing fees, which can be as high as 3% per transaction but also aligns with the interests of cash-paying customers who appreciate the cost savings. By openly communicating the financial advantages of dual pricing, businesses can encourage more customers to opt for cash payments, further enhancing their profit margins.

Additionally, businesses adopting dual pricing are in a unique position to maximize profits by strategically promoting cash payment incentives. For instance, offering a direct discount for cash transactions not only appeals to cost-conscious consumers but can also lead to increased cash flow for the business. In an economy where every percentage point counts, being proactive about payment strategies can fortify a company’s financial standing and customer base. As businesses learn to navigate the complexities of dual pricing, they will find that the benefits extend beyond just reduced fees, fostering loyalty and satisfaction among their clientele.

Legislative Trends Supporting Dual Pricing Strategies

The recent legislative support for dual pricing in regions such as Florida signals a pivotal shift in the way businesses can approach pricing strategies. Laws that allow merchants to differentiate prices based on payment methods reflect a growing recognition of the financial challenges faced by businesses due to high credit card fees. By enabling dual pricing, lawmakers are providing businesses with the flexibility to implement a pricing model that can enhance profitability without alienating consumers. This legal backdrop paves the way for more businesses to adopt innovative pricing strategies that cater to varying customer preferences.

Moreover, legislative advancements in supporting dual pricing highlight a growing trend toward consumer empowerment in financial decisions. With clearer pricing structures, customers become more informed about their payment options and can choose the most economical route for their purchases. This empowerment not only encourages cash transactions but also motivates consumers to actively seek alternatives that benefit their budgets. As the acceptance of dual pricing continues to spread, businesses should stay informed about legislative developments to navigate these changes successfully and take advantage of the opportunities they present.

Implementing Dual Pricing: A Step-by-Step Guide

Transitioning to a dual pricing model requires careful planning and execution to ensure its effectiveness. The first step for businesses is to evaluate their current pricing strategies, considering factors such as customer demographics, payment preferences, and the overall competitive landscape. This analysis helps determine whether dual pricing fits the business model and identifies the potential benefits, such as maximizing profits through reduced credit card fees. It’s essential that businesses conduct thorough market research to understand how their consumer base might respond to these changes.

Communication is another crucial aspect of a successful dual pricing implementation. Businesses must clearly articulate the value behind the dual pricing strategy to customers, emphasizing the benefits of cash payment incentives. This includes not only the price difference but also the advantages of supporting local business operations by opting for cash transactions. Additionally, updating point-of-sale systems to accommodate dual pricing is vital for a seamless transition. Training employees to effectively inform and assist customers as they navigate the new pricing structure ensures that the implementation process runs smoothly, ultimately leading to enhanced financial outcomes.

Challenges of Dual Pricing and How to Overcome Them

While dual pricing offers significant advantages, it is not without its challenges. One of the primary concerns for businesses is consumer resistance, particularly from customers who prefer credit card transactions due to convenience and rewards offerings. To counter this, businesses should strategically inform customers about the rationale behind dual pricing and the savings associated with cash payments. It’s essential to highlight the long-term benefits, such as lower prices for cash transactions, which can help shift consumer behavior over time.

Moreover, legal compliance must also be prioritized when implementing dual pricing. Each region may have specific regulations regarding pricing strategies and advertising these prices. Businesses need to conduct thorough research and possibly consult legal professionals to ensure that their dual pricing structures comply with local laws. By proactively addressing these potential challenges, businesses can smooth the transition to a dual pricing model and fully capitalize on its benefits while maintaining customer satisfaction.

| Key Point | Details |

|---|---|

| Definition of Dual Pricing | A pricing strategy where different prices are charged based on the payment method, encouraging cash payments over credit card usage. |

| How It Works | Cash customers pay a lower price, while credit card users pay slightly higher to cover processing fees. For example, $100 for cash vs. $103 for credit card payments. |

| Industry Trends | Growing adoption by SMEs and legislative support in various regions like Florida, reflecting a shift towards flexible pricing strategies. |

| Benefits | Reduced credit card fees, increased cash flow, and enhanced customer transparency. |

| Challenges | Potential customer resistance and legal compliance issues regarding pricing structures and displays. |

| Implementation Steps | Evaluate business needs, communicate the pricing model, update systems, and monitor customer feedback. |

Summary

Dual pricing emerges as a strategic approach that offers businesses the ability to manage credit card processing fees effectively. By differentiating prices based on payment methods, companies not only retain more profit but also encourage customers to consider cash transactions as a viable option. As more businesses adopt this model, understanding its benefits and challenges becomes essential for staying competitive. Adopting dual pricing not only responds to rising operational costs but also represents a forward-thinking strategy in today’s dynamic economic environment.

Frequently Asked Questions

What is dual pricing and how can it help reduce credit card processing fees?

Dual pricing is a pricing strategy where businesses charge different prices based on the payment method used. This approach can help significantly reduce credit card processing fees by encouraging cash payments, therefore maximizing profits. For instance, customers who pay with cash may benefit from a lower price compared to those paying with credit cards, thus offsetting the businesses’ transaction costs.

How can implementing dual pricing maximize profits for my business?

Implementing dual pricing can maximize profits by reducing the financial burden of credit card processing fees. When businesses encourage cash payments through lower prices, they improve cash flow and retain more revenue. As more consumers choose cash over credit due to the price difference, businesses can enhance profitability while maintaining price competitiveness.

Are there legal considerations to keep in mind when using dual pricing?

Yes, businesses must be aware of local laws regarding dual pricing practices. Compliance with pricing display regulations and ensuring transparent communication with customers is crucial. Some regions support dual pricing by legislation, while others may have restrictions, so it’s essential to consult local guidelines before implementing this pricing strategy.

What advantages does dual pricing offer for encouraging cash payment incentives?

Dual pricing provides clear cash payment incentives by offering lower prices to customers who choose to pay in cash instead of credit. This strategy not only reduces credit card processing fees but also nurtures consumer awareness about payment options, fostering a cash-friendly environment that supports better cash flow management and profitability for businesses.

Minimizing operational costs is crucial for businesses aiming to maximize profits, and one significant expense that can eat into margins is credit card processing fees. Many small businesses often overlook these fees, which typically range from 1.5% to 3% of each transaction. However, adopting a strategy that allows for 0% credit card processing fees can dramatically transform a business’s financial landscape. This can be achieved through the implementation of certain payment models, such as charging customers a service fee for using a credit card or incentivizing cash payments with discounts. By effectively managing these credit card fees, businesses can redirect those savings into growth initiatives, improving overall profitability.

To enhance profit margins, businesses are increasingly exploring various pricing strategies, particularly around credit card usage and fees. One innovative approach is to offer cash payment incentives, encouraging customers to pay in cash instead of credit. This not only effectively eliminates credit card processing fees associated with card transactions but also fosters customer loyalty by providing them with a tangible benefit—a discount or lower price for opting to pay cash. Such strategies not only improve cash flow but also help businesses retain a greater percentage of revenue, thus leading to improved profitability.

In addition to implementing cash payment incentives, it is crucial for businesses to analyze their overall pricing strategies in light of credit card fees. Utilizing data-driven insights to understand customer behavior and payment preferences can guide businesses in structuring their pricing accordingly. By offering tiered pricing based on payment methods or introducing minimal surcharges for credit card transactions, businesses can ensure they cover any associated costs while still providing value to their customers. This balanced approach allows businesses to maintain competitiveness in the market and optimize profit margins.

Understanding credit card processing fees is essential for any business aiming to boost profitability. These fees can significantly impact the bottom line, yet they are often not fully on the radar for most entrepreneurs. To address this, businesses can conduct a thorough analysis of their transaction volumes and fee structures, comparing different payment processors to find the most advantageous rates. Additionally, transparency about these fees with customers, perhaps by illustrating the cost breakdown on receipts or during the purchasing process, can help align expectations and encourage more cost-effective payment methods.

Ultimately, adopting smart pricing strategies focused on managing credit card fees, alongside offering incentives for cash payments, enables businesses to not only preserve their profit margins but also create a loyal customer base. By prioritizing cost efficiency and customer empowerment, businesses can transform potential financial burdens into opportunities for increased revenue and long-term sustainability.

In today’s competitive market, dual pricing presents a revolutionary approach to manage credit card processing fees efficiently. By understanding that different payment methods carry varying costs, businesses can optimize their pricing strategies. This not only helps in absorbing or offsetting the credit card fees but also allows companies to maintain pricing flexibility, catering to both cash and credit customers. As a business owner, leveraging dual pricing not only empowers you to boost your profit margins but also creates a transparent relationship with your customers, who can see the financial implications of their payment decisions.

Implementing dual pricing also aligns with broader trends in consumer behavior, as an increasing number of consumers are becoming more mindful of transaction fees associated with credit cards. This conscious shift invites businesses to capitalize on cash payments, which can enhance liquidity and minimize dependency on credit card providers. Additionally, as legislation evolves to support such pricing practices, entrepreneurs have the opportunity to engage in a profitable model that resonates with both current economic challenges and emerging consumer preferences.

Furthermore, adopting a dual pricing strategy can lead to improved customer relationships. By openly communicating the rationale behind the pricing structure, businesses can foster a sense of trust and understanding with their clientele. This transparency can mitigate negative reactions from customers who might initially resist the concept of dual pricing, as it displays a commitment to fairness. Engaging customers in this dialogue allows businesses to position themselves as customer-centric, ultimately leading to increased loyalty and repeat patronage.

The successful implementation of dual pricing requires careful planning and ongoing evaluation. As merchants navigate the transition, it’s crucial to remain responsive to customer feedback and market dynamics. Monitoring sales trends, consumer preferences, and legislative changes will inform necessary adjustments to the dual pricing model. By staying adaptable and informed, businesses can not only mitigate credit card processing fees but also remain competitive in a rapidly changing economic environment.

In conclusion, dual pricing is more than just a strategy to combat escalating credit card fees; it represents an evolving business paradigm that encourages transparency, fosters customer relationships, and enhances profitability. As consumer preferences shift and operational costs rise, exploring dual pricing could be your ticket to not just surviving, but thriving in an increasingly competitive landscape. Embrace the opportunity to innovate your pricing strategy today and take the first step toward a more profitable future.